Updates: SNOW 4Q24 - Leadership Change, Competition, GTM, AI Talent War (Pt.2)

Summary

- In Part 2 we dive into SNOW's products, both its core CDW and its new products related to handling unstructured data and AI/ML workloads.

- Before the latest ER shock, SNOW was perfectly priced as investors fully believed in the $10bn revenue by FY29 story.

- Now that prospect has diminished due to growth reacceleration uncertainties, SNOW offers some but not huge upside.

- Note: we have fell behind the cadence we like to deliver recently, though we do have a PLTR report ready to be published over the weekend.

SNOW & AI

Two strategic issues for SNOW's continued CDW penetration and resulting growth relate to the open stack and AI. SNOW has been working hard to make its platform more open and supportive of ML/LLM workloads. To make it more open, SNOW provides support for Iceberg, but it also means that it is going to lose 5%-10% of its revenue, because many Iceberg users will opt to use AWS Glue instead of SNOW for managing the Iceberg + object storage compatibility.

In terms of GenAI/LLM, for most enterprises, they won't train their own model from the ground up, but instead take a open-source base model and train that. A typical enterprise will likely spend 40% on fine-tuning the base model, of which, 10-15% is spent on data preparation and making it highly curated, and 60% on inferencing. Right now, SNOW's CDW only makes money in that data curation part.

The good side is that SNOW's CDW owns the most curated data that are critical for model training. Compared to others like Databricks that have a data lake that has files dumped without formatting or any data quality controls, SNOW's CDW has better catalog, governance, and structure to enable better fine tuning. As explained in our State of GenAI report, when fine tuning a base model, you don't need a huge amount of low quality data, like what is the case during the pretraining phase. Instead, you need a smaller amount of high quality data. That's where SNOW has the most valuable gold mine. Even if you want to use unstructured data for training a base model, you still need to label it, mask privacy-related sensitive data, and target and identify the dataset to avoid duplication - these are all in SNOW's favour.

The downside is that SNOW has been focusing more on CDW, whose core users are non-technical business analysts. SNOW has less knowhow and product research in ML and obviously DL & LLM. Due to its CDW focus, although it offers support for unstructured data saving, most customers keep unstructured data in date lakes external to SNOW, and only load curated data to SNOW. And most of them maintain data lakes in Databricks where data scientists can play with unstructured data and try new experiments more freely without fine governance control and strict schemas. Databricks controls the ML part of data preparation, whereby unstructured data is transformed to structured data, and it has acquired MosaicML to boost its small parameter foundation model offerings and LLMOps platform. These offers will capture a majority of AI spending as opposed to SNOW on CDW and SQL.

The general IT spending in 2023 wasn't rosy; overall spending has been slightly up at ~3%. But for non-AI vendors, it has been the worst year. CFOs and CIOs need to find additional budget for the urgent GenAI initiatives, and to do so they need to cut spending in other areas of IT. As SNOW's core CDW product has less direct link to AI, SNOW needs to expand into ML and data science, and DL/LLM to capture the AI opportunity.

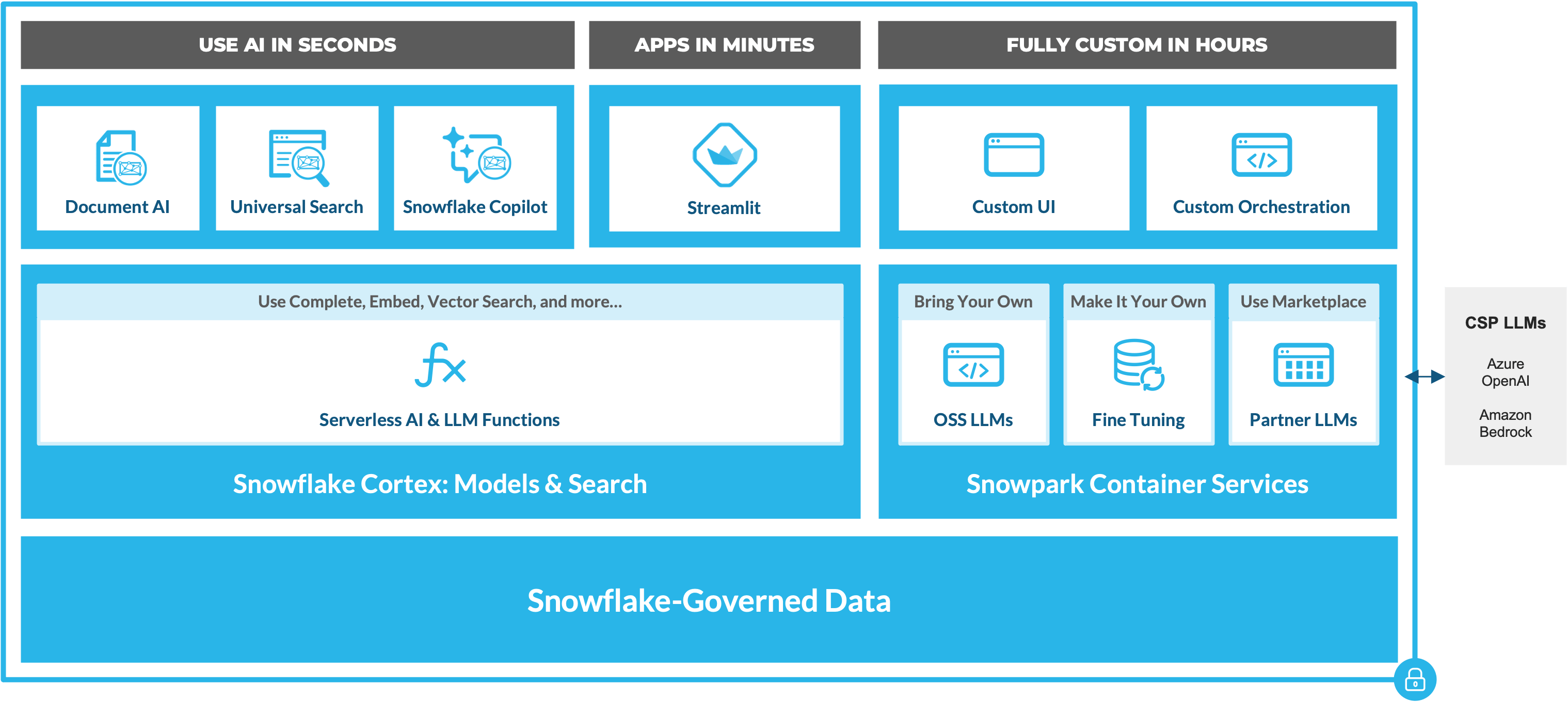

Snowpark is SNOW's ML product that allows data science and ML transformation to be carried out within the SNOW platform, instead of processing unstructured data outside of SNOW and then loading it into SNOW.

Cortex is SNOW's AI platform that provides both out-the-box AI-as-a-Service and PaaS for companies to build their own AI apps and services.

Snowpark Container Services (SPCs) provides lower level customization for sophisticated customers who want to run their own codes, customize and fine-tune models, and deliver value in their own ways.

Snowpark

In June 2023, SNOW announced GA of Snowpark, the private preview of SPCs, and associated tool chains just shortly after the Neeva acquisition.

{kind=link}