Updates: PANW 2Q24 - The New Platformization Play And Its Impact On Competitors

Summary

- Following the 2Q24 call, PANW gapped down ~26%. Unlike other gap downs in the past, this was driven by management's radically new strategy as opposed to an earnings miss.

- Contrary to what the market has priced-in, the new platformization strategy is very likely to put huge pressure on existing public competitors and smooth out many startups.

- It will unlock the potential of various PANW BoB products that have thus far been capped by customer restraints.

- Similar to the gap down of other BoB and high quality names, PANW's stock has now de-risked and its expected return has increased substantially.

- The share price is now in the fair value range, but we see substantial long-term upside for our bull case scenarios, which we believe a quite likely to prevail.

Related companies: MSFT, CRWD, ZS, FTNT, AVGO, HPE, JNPR, Netskope, Cato Networks, Versa Networks, Island.io, Wiz Security, Orca Security, Aqua security, Lacework, Snyk, Torq, Tines.

https://twitter.com/convequity/status/1761029075681083684

Recapping price action

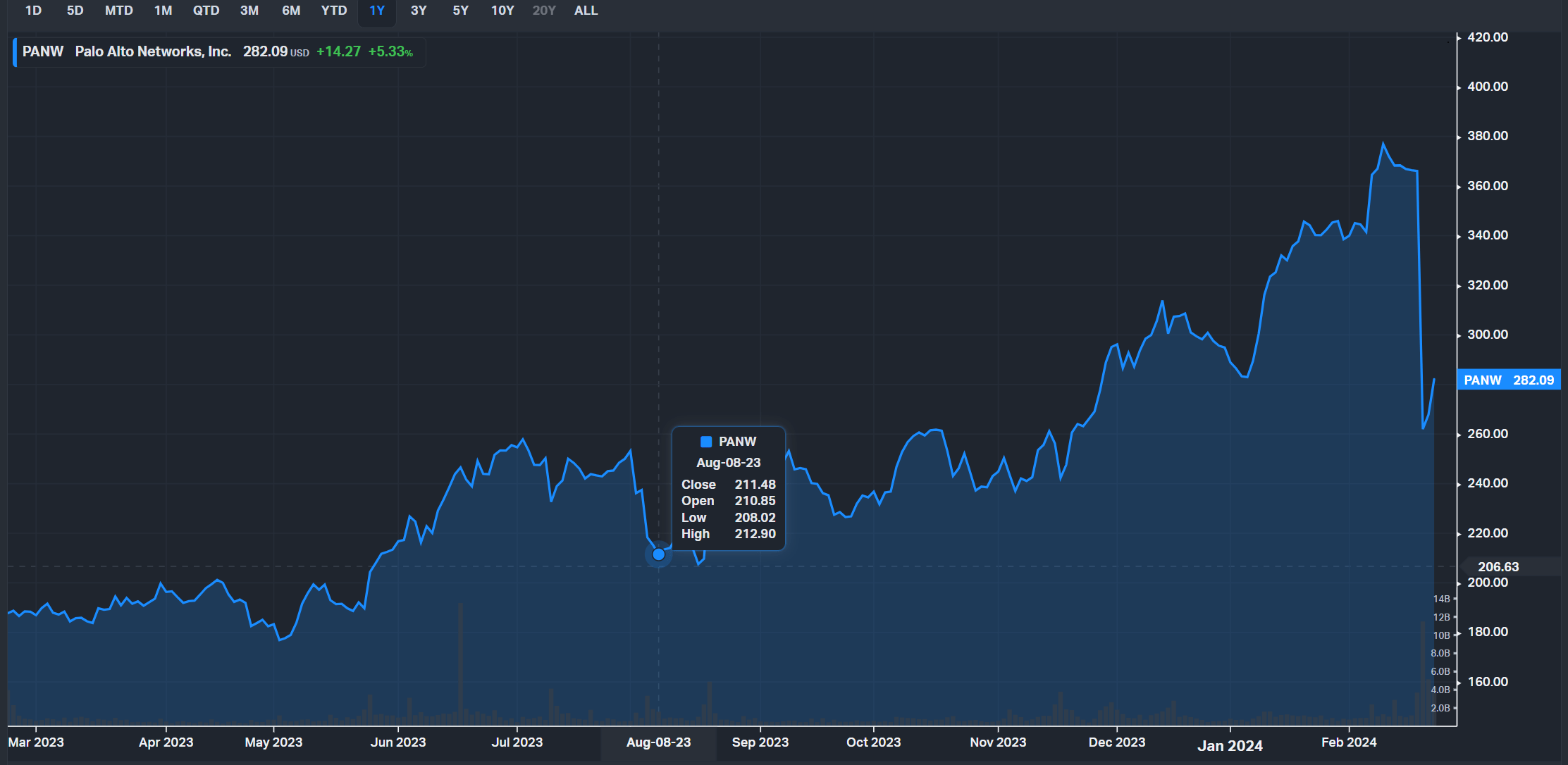

The latest 2Q24 ER created a ~26.5% gap down due to a $600m guide down for FY24 billing due to PANW's latest 'platformization' pivot. However, it is important to note that on a 3M basis, the stock is still up by 7% (as of Friday's close on 23rd Feb 2023).

In many ways, the 2023 year-end run-up for PANW has been too excessive in both its velocity and investor sentiment. In recent weeks, we are increasingly seeing virtually every bear turning into a bull, and cherishing the same thing again and again, including SASE, cloud security, and SecOps strength. It is often a strong risk signal when there is no bear on the street, and new bulls are unsophisticated trend followers joining the game because of the nice looking chart, surface-level thesis, and less considerate of the valuation.

On a higher level, we have seen cybersecurity as a category really broaden out to mainstream investors as we entered 2023, a period during which many stock market areas continue to slowdown, while cybersecurity remains the top priority item on most of BB investment bank's CIO and channel surveys. Many generic investors have increased their allocation in cybersecurity substantially, and with the story quickly unfolding from a recession + bear market to a rate-cut + melt-up market, investors need to put their excess of ~$10tn dry powder to work. Hence, tons of investors join the ride now with more of a top-down allocation rather than a bottom-up stock picking methodology. One particular anecdote is that Brad Gerstner of Altimeter mentioned PANW on numerous occasions putting it in the same bucket as SNOW and META. This shows how consensus PANW has become. At the 52-week high of $380, up from low of $176, is a ~116% return that reached a peak market capitalization of over $100bn.

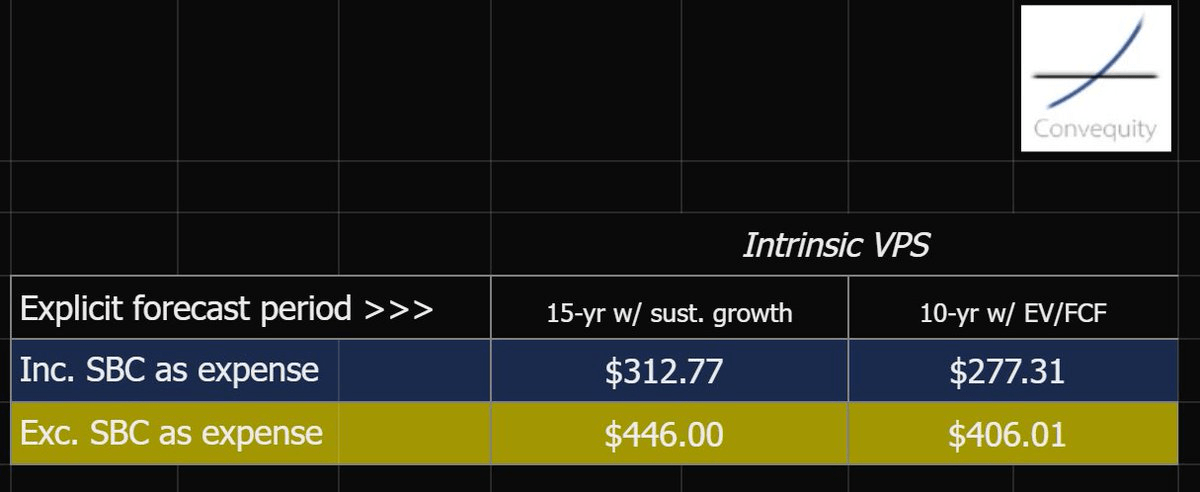

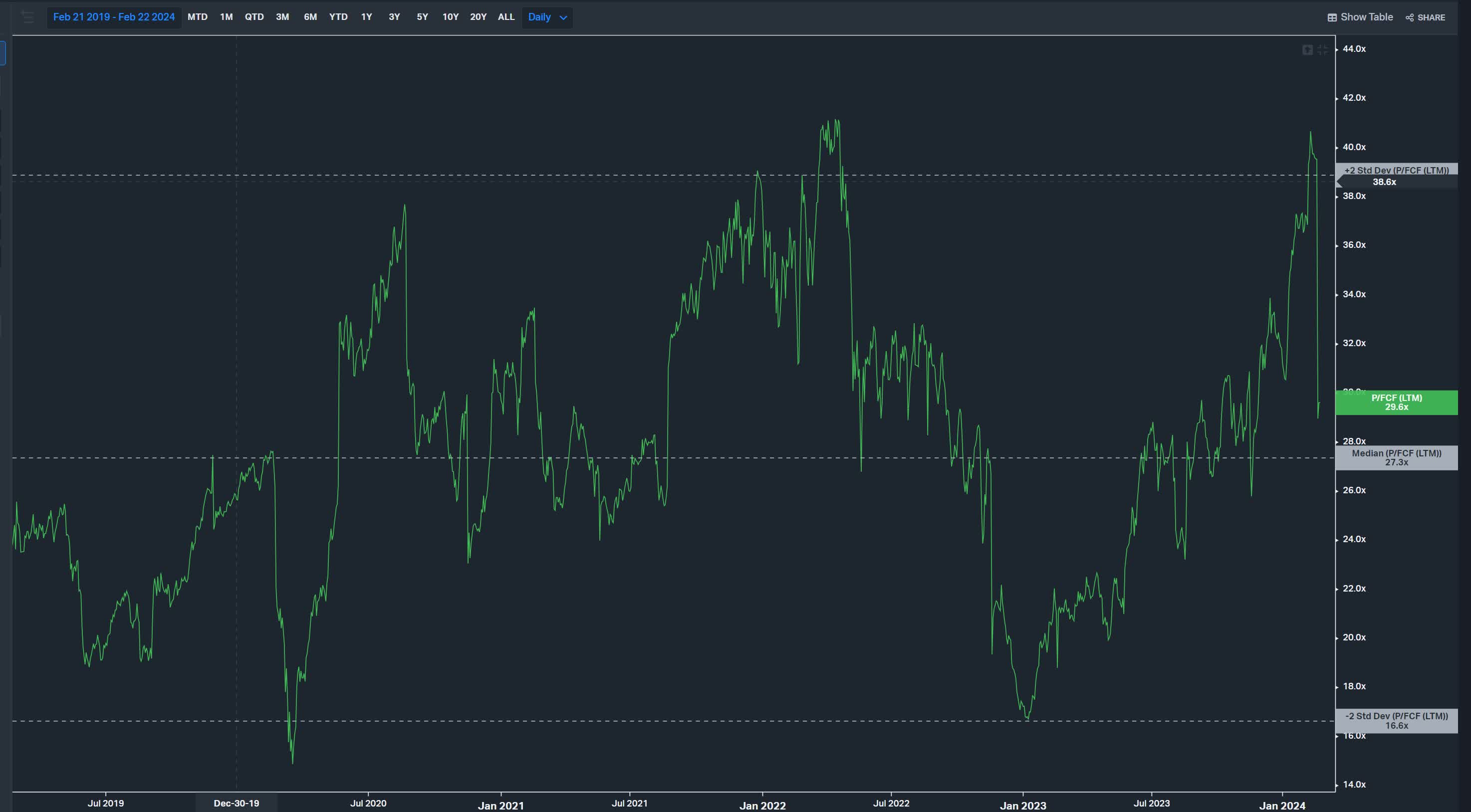

As we analyzed in our previous PANW update on 22nd Aug 2023, the valuation for PANW back then wasn't too cheap nor too expensive. It was fair-to-slightly premium, especially if you consider the trend of the 5Y P/FCF multiple. However, the recent melt up has pushed the valuation above 2 std dev. And obviously, the price rose higher than our price target on our baseline DCF valuation.

Coming into 2023, we saw many companies give conservative guidance, and then gradually adjusted their guidance upwards. Then analysts followed with higher expectations that eventually front runs the guidance upward revisions. Then with pumped expectations, it is harder for management to make beats but misses. This often comes with high valuations and price-to-perfection scenarios that investors often justify by saying this is the perfect stock that deserves the premium valuation and this is the stock that we must hold no matter where the valuation is because of FOMO sentiment.

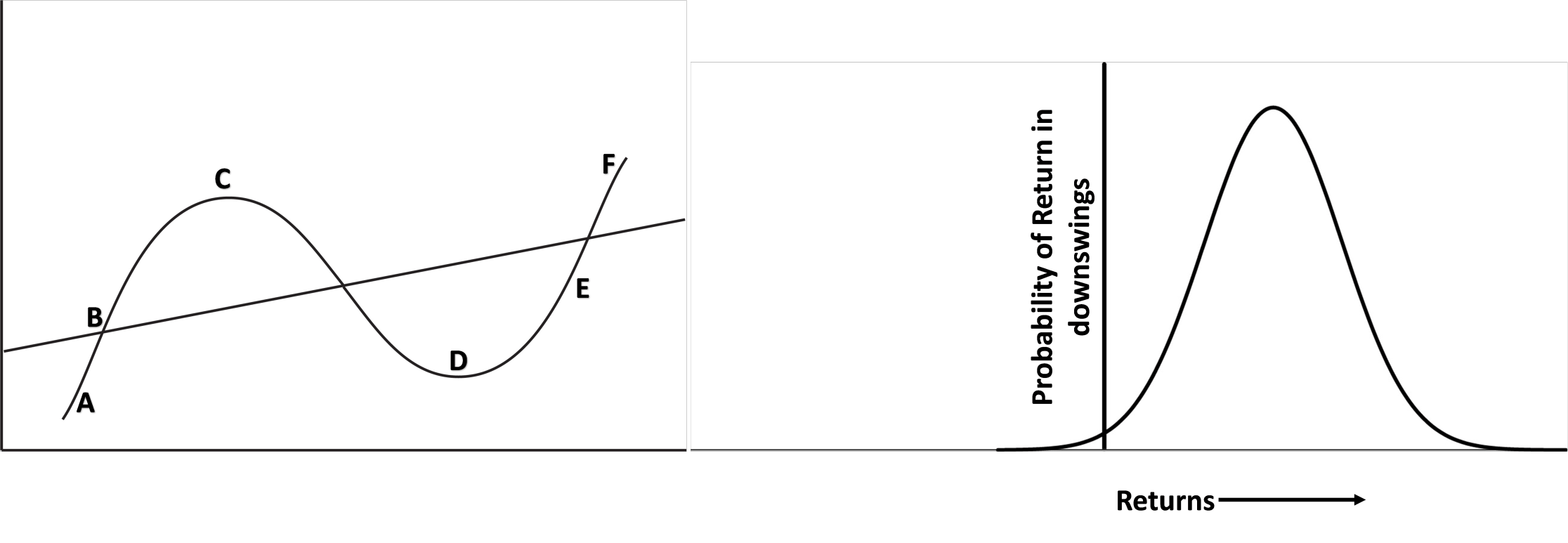

Though, investor sentiment and the associated valuation multiples never stay in a happy medium, and instead exhibit the movement of a pendulum with ups and downs, as conceptualized by Howard Marks.

Therefore, it is understandable that the market voted PANW down post-ER. But from the bottom-up perspective, we disagree with the market, just like what we did in early 2020 when we started PANW coverage believing it was highly undervalued due to investor misunderstanding and surface-level research by the investment community.

Understanding Platformization

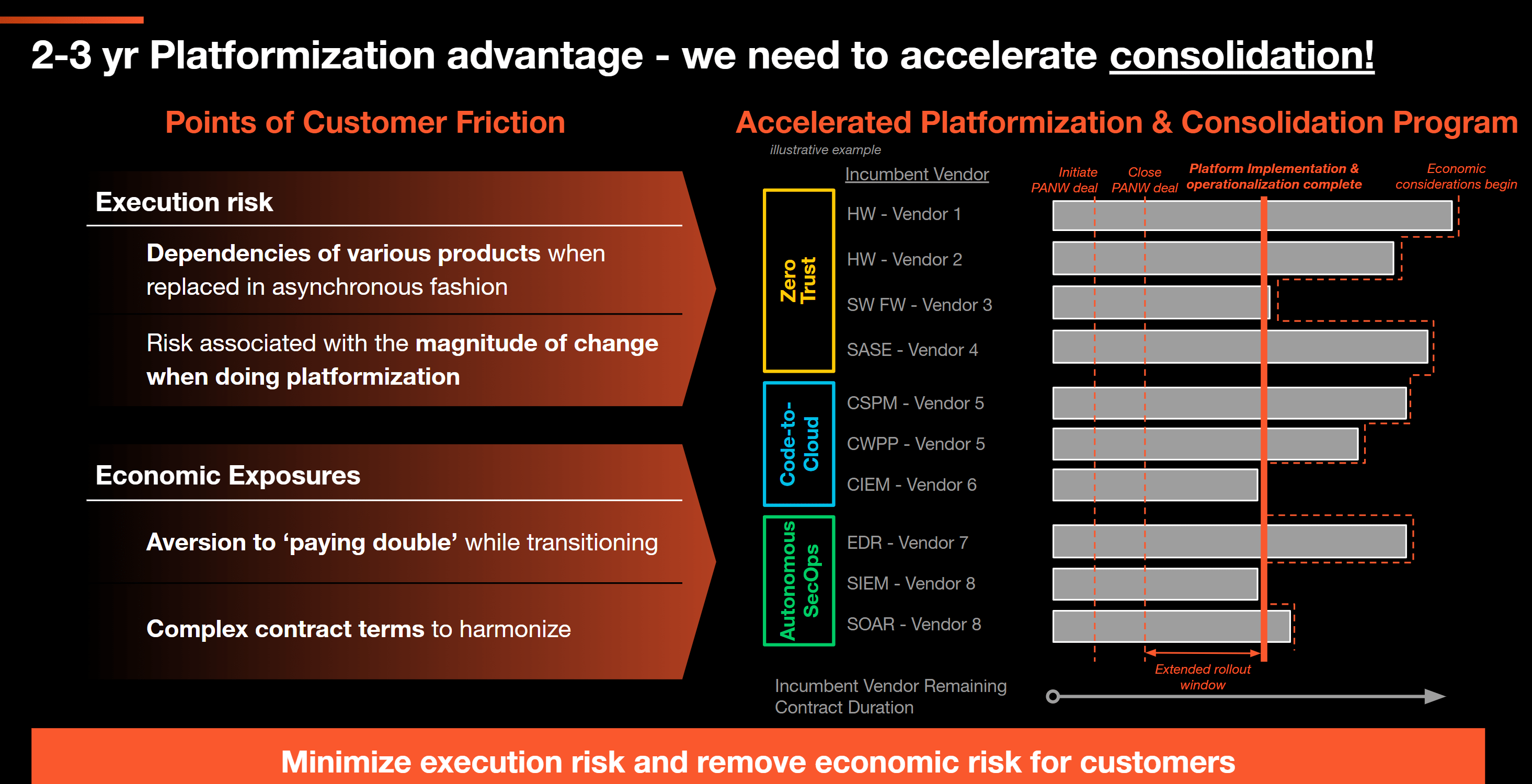

The biggest surprise to investors in the 2Q24 ER is the incoming strategic shift. PANW will be providing its platform bundle for free when an existing customer is facing deal timing issues, and cannot deploy PANW's other components immediately. As the management has explained, and we believe 100% with observation, the S&M practices in cybersecurity are very nasty. And in many times, or 80% of deals, the win is not attributed to the purity of the technology or product, but is simply an S&M win. Many vendors with weak products can win with strong marketing, mindshare, distribution, existing relationships, channel partnerships, the ability to provide additional product bundles for free or at 1/10 of the price, or even simply selling the renewal below COGS to keep a customer.

PANW has lost many mega deals due to timing associated with the varied remaining contract durations of point solutions.

It is very often that one existing customer of PANW may find its other solutions very attractive, and PANW's strong S&M machine is able to sell it to stakeholders. However, most customers have existing solutions in place, and because of the recent operating efficiency push and CFO-led budget reviews, they cannot simply buy PANW's solution, and let the remaining 2-year license from its incumbent solution fritter away without any ROI. And when it finally comes to the end of the existing license, the existing provider will learn that PANW is competing on this solution, and they will do whatever they can to keep the customer, even if that means selling the renewal license at uneconomic prices.

Point solution product vendors can also undercut PANW by selling the product at lower prices and win customers with deeper focus in one particular niche. From a TCO perspective, PANW's overall platform and bundle can provide more effective security at lower prices. But most customers prefer to negotiate with PANW on a per product basis due to budget timing and the way the procurement process works, which is mostly because we have never before seen a true comprehensive cybersecurity platform. But now there is PANW, and its platform is one-of-a-kind, so it needs a new way to break into customers and sell to them more effectively.

In addition, this is also the time when PANW has the peak relative advantage vs. peers in many fields, including SASE, CNAPP, SecOps, and others. For instance, PANW's Talon, the startup acquired for its secure enterprise browser, leads the rest of the pack by a wide margin (excluding Island.io), its CNAPP is the strongest on the market, and its XSIAM is a one-of-a-kind leading innovation, not only for public peers but even for seed stage startups who are typically the most innovative and cutting edge. So it makes 100% sense for PANW to provide the platform bundle to existing customers who have exhibited an initial interest in adopting other platform components but do not have their remaining contract durations well-aligned, have near-term budget constraints, and have not yet had the time to do a full platform-level TCO evaluation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}