Updates: Monday 4Q23 - Continued Great Execution

Summary

- MNDY continues with excellent execution at the top and bottom lines.

- During this update we make a number of comparisons between MNDY and ASAN to help investors better understand MNDY's strengths.

- We dive into mondayDB and how it may impact the vendor's gross margins. We also review MNDY's other promising products that compliment its core work management platform.

- Relatively speaking, MNDY's stock looks attractive but the DCF valuation indicates fair value range, suggesting the market might be getting frothy among MNDY's high-flying peers.

For a deep dive into MNDY check our previous update report.

4Q23 Overview

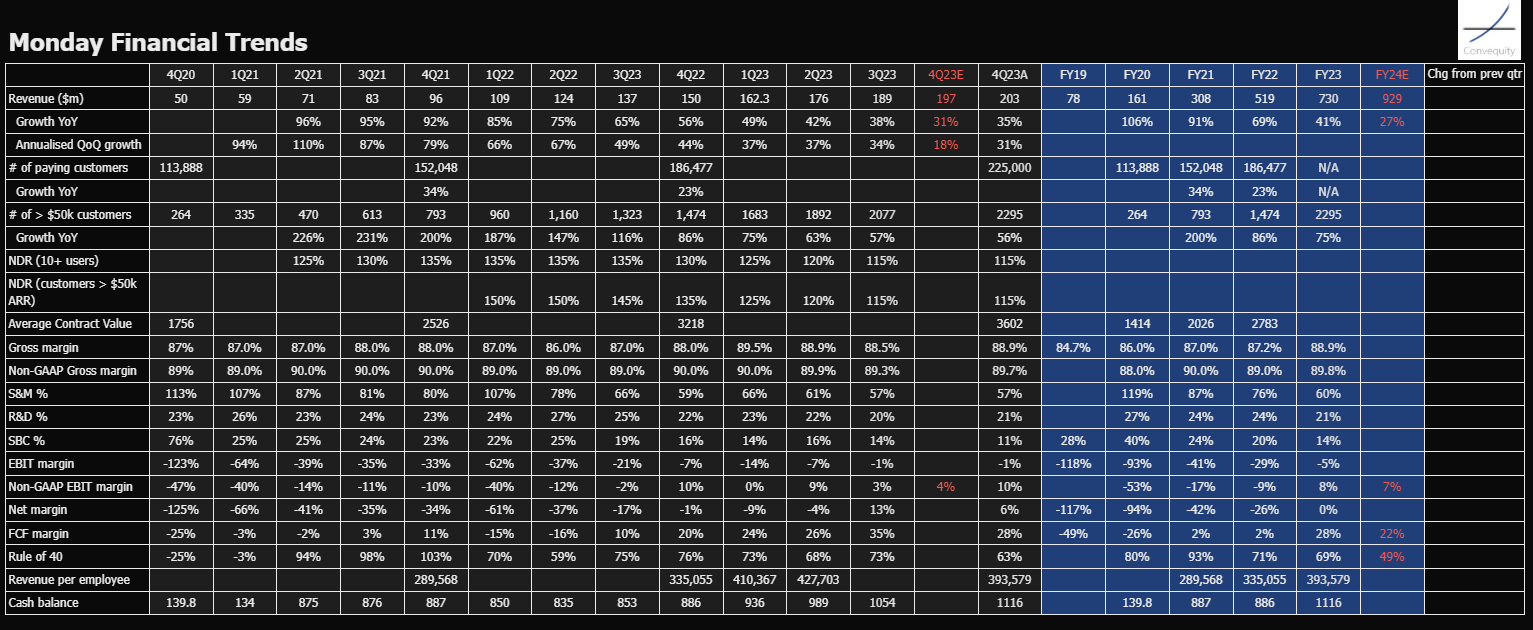

MNDY’s 4Q23 revenue was $203m (YoY 35% growth) vs. guidance of $197m (YoY 31% growth). Sequentially, the growth was 7.4%, translating to an annualized QoQ growth rate of 31%, which is high among SaaS stocks in the present climate. 4Q23 non-GAAP EBIT was $21m (10.3% margin) vs. guidance of $7m (4% margin), compared to 4Q22 of $14.3m (10% margin). The general takeaway is that MNDY continues generating solid growth with notably less decay versus many SaaS peers while also finding increasing operating leverage.

MNDY Financial Trends & DCF Valuation

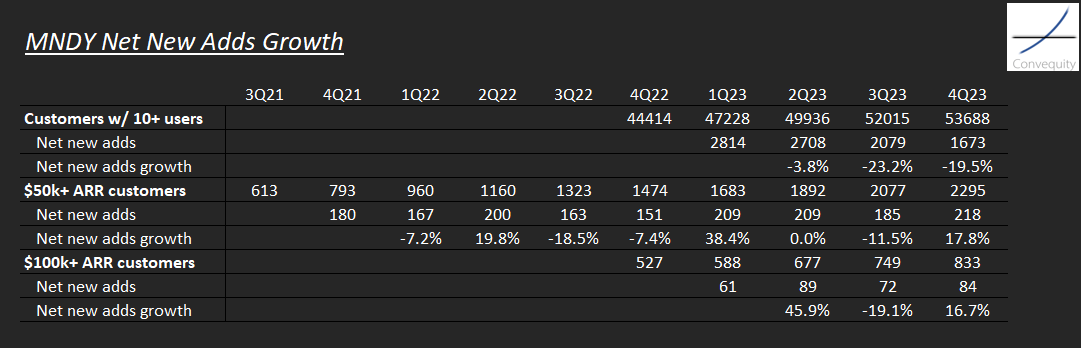

MNDY’s net new customer adds growth was also solid in 4Q23. This metric is very bumpy as it is a second derivative, however, it’s assuring to see strong positive net adds growth for the $50k+ and $100k+ ARR customer categories. MNDY has been reporting the actual number of $50k+ customers since its IPO but only started reporting the actual numbers (not just the NDR) of $100k+ customers and 10+ users customers in 4Q23 (and disclosing the prior 5 quarters), which is why the table below is showing many blank cells.

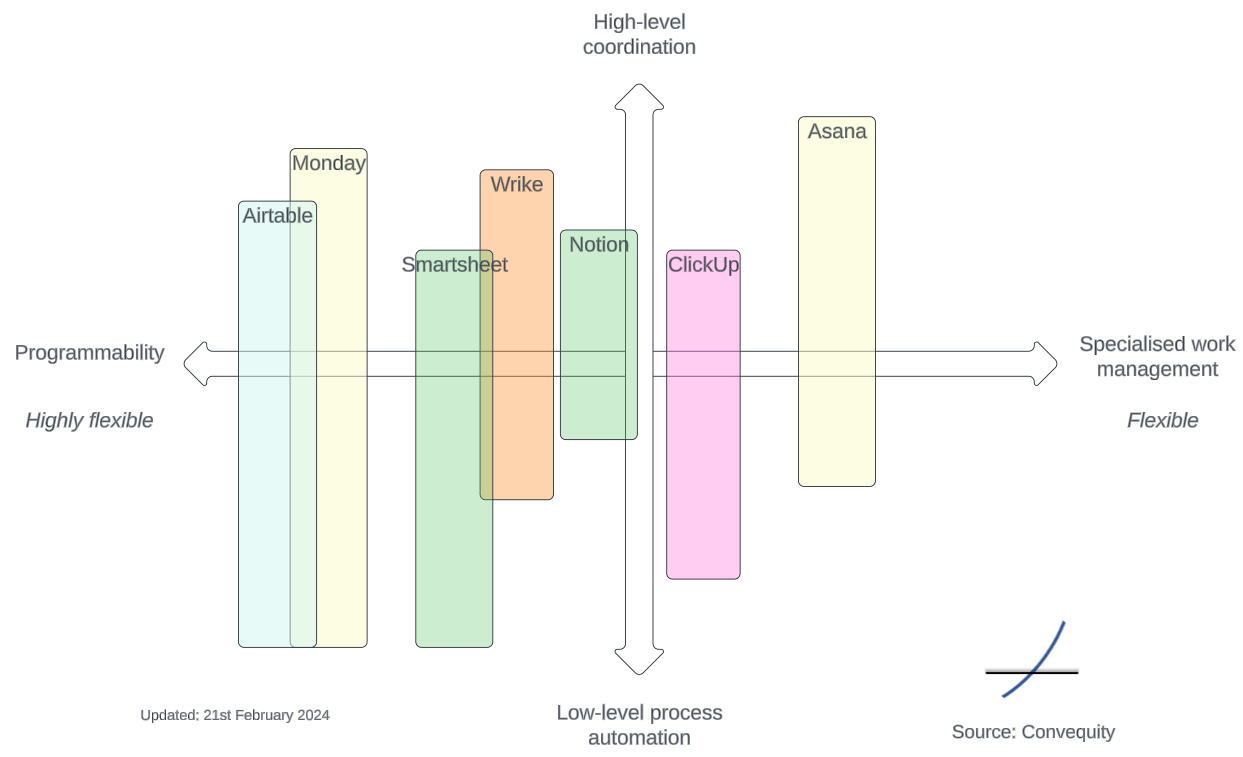

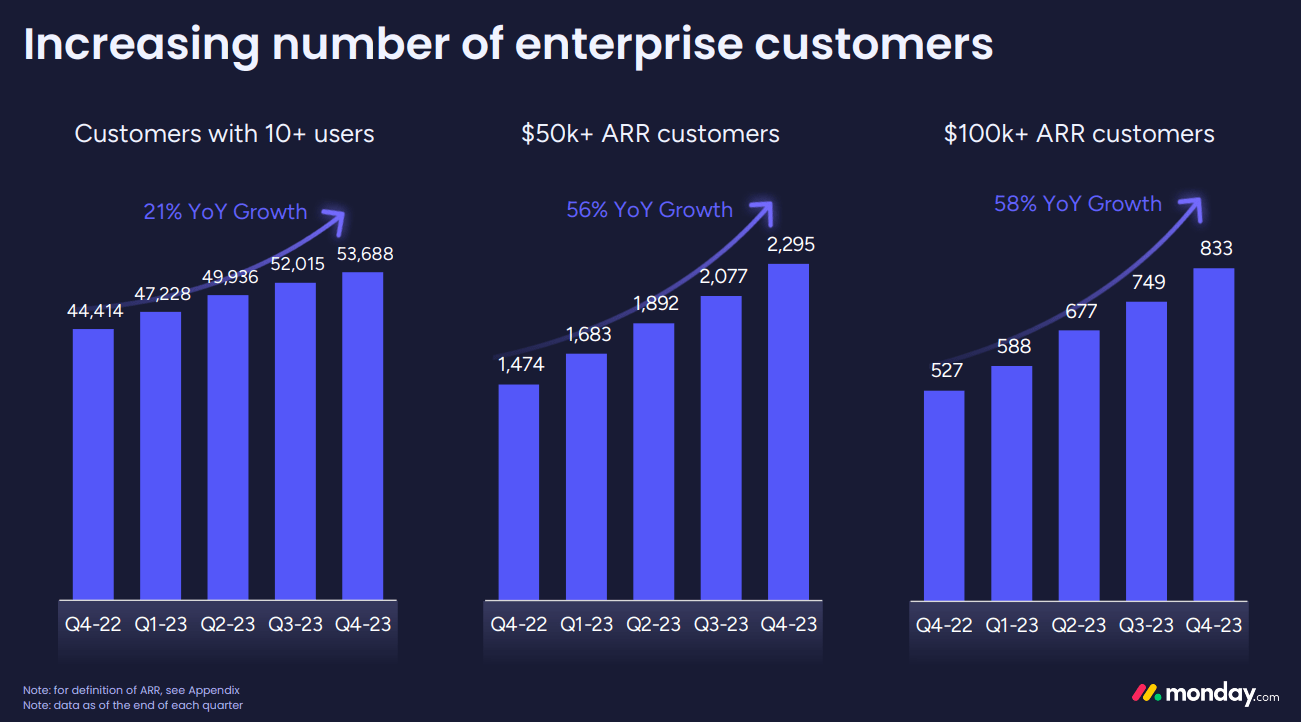

It’s interesting to note that MNDY currently has 253 more $100k+ enterprise customers than ASAN (833 vs. 580) – note that this is based on MNDY’s 4Q23 that ended 31st December, which is two months later than ASAN’s 3Q24 that ended 31st October. Nonetheless, this is a big gap considering the two companies are in the same market, have the same business model, and have similar TTM revenue levels (MNDY $730m, ASAM $632m). The greater number of enterprise customers with MNDY is attributed to MNDY’s broader use cases that span across the low-level processes and the high-level coordination areas of work management. In contrast, historically ASAN has been a lot less focused on the low-level process area, and extra focused on the high-level coordination, albeit they have been targeting the former more recently.

MNDY’s greater focus on low-level processes, i.e., tasks and workflows, has enabled the vendor to gain detailed understandings of how certain workflows operate, which in turn has given MNDY the confidence to release new products such as monday CRM, monday Dev, and soon-to-be launched monday Service (more on these later). On the contrary, ASAN hasn’t released any products tailored to specific workflows within the realm of work management because they are focused too much at the higher levels, resulting in the vendor providing great coordination capabilities across departments but little hands-on knowhow of low-level processes.

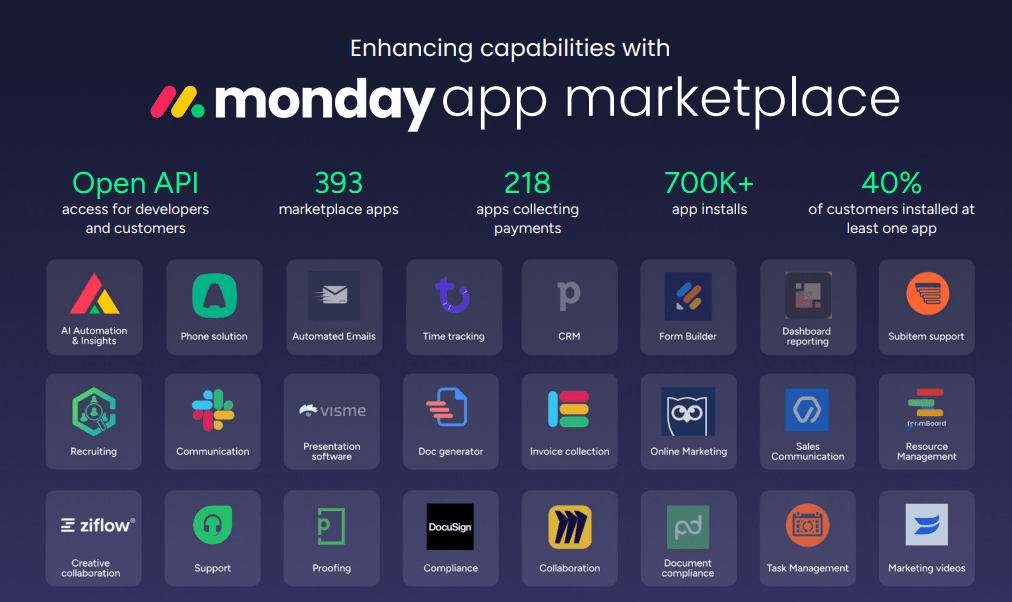

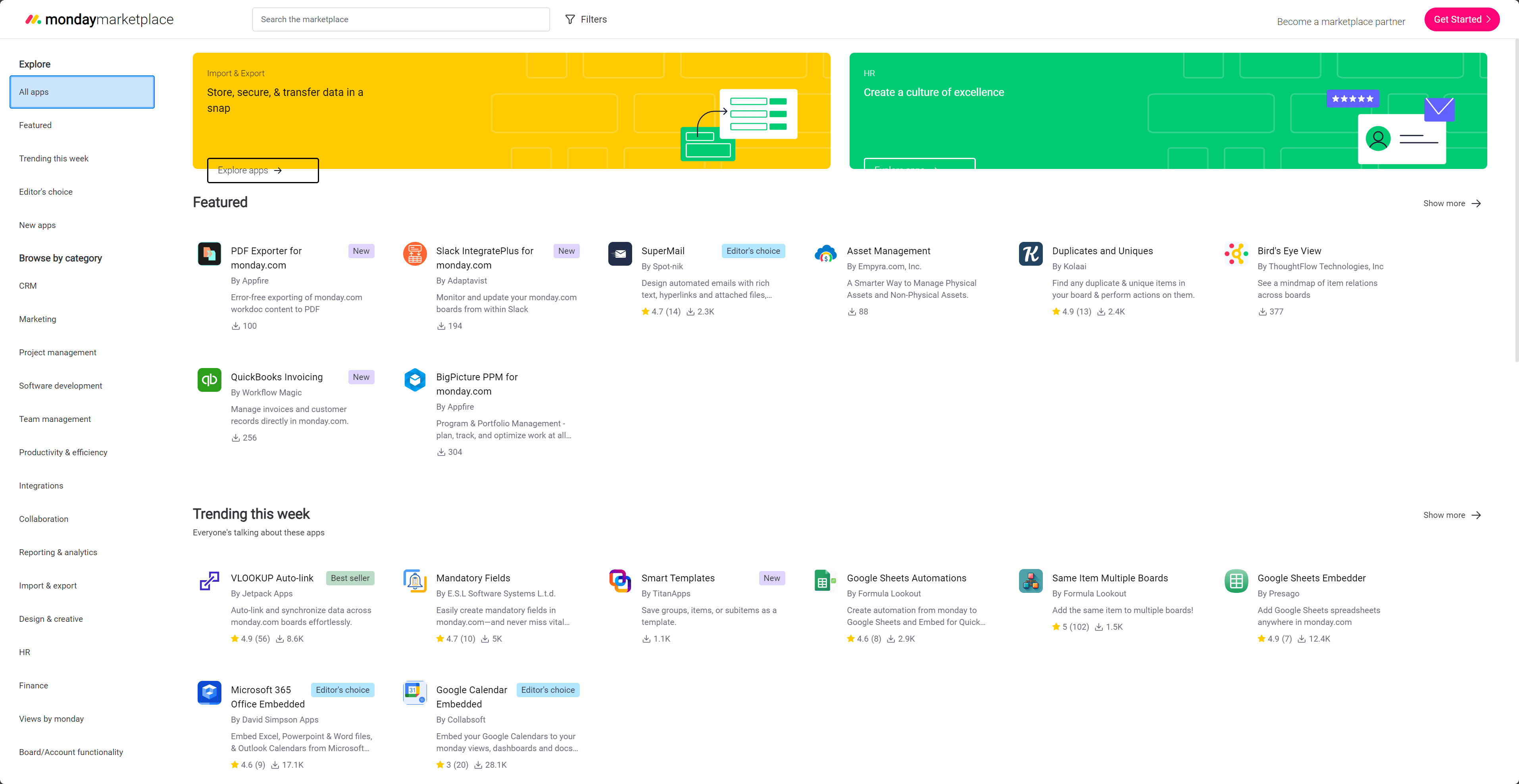

You will observe in the diagram above that we also categorize MNDY as way more flexible than ASAN - MNDY transcends beyond specialized work management whereas ASAN largely stays with the work management domain. This is because from early on MNDY’s priority has been to make itself an easy-to-use no/low code platform capable of empowering users to create a wide range of automated workflows and entire applications. This has not only attracted more enterprise customers but also appealed to hundreds of partners, many of which have built their entire consultancy business by developing custom apps for their customers on the MNDY platform. This trend has snowballed into a very vibrant Monday Marketplace.

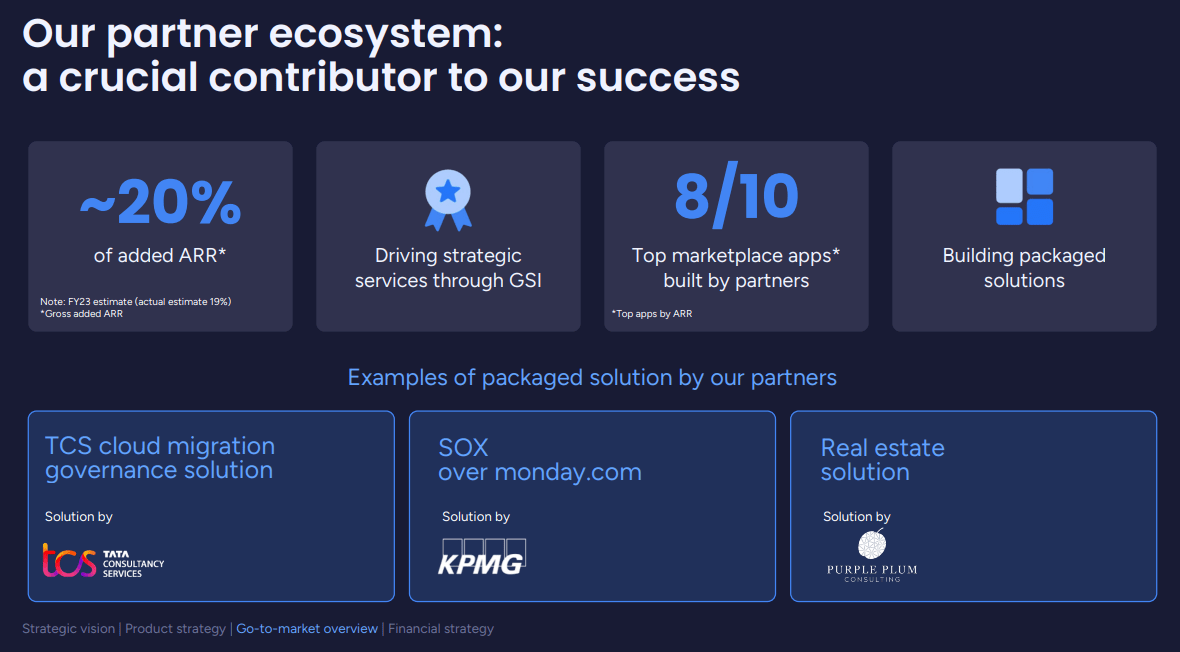

ASAN also provides no/low functionality, but they started later and haven’t invested as heavily as MNDY. As a result, with ASAN you can develop custom workflows but it is not flexible or programmable enough to build highly complex workflows or entire new applications. This level of no/low code programmability is the catalyst for attracting this high number of partners, some old and established (e.g., KPMG), and some who have based their business almost entirely by creating MNDY apps for customers (e.g., Omnitas Consulting). These partner-made apps can also be sold on the marketplace. In effect, this no/low code programmability has created a flywheel effect for MNDY, because as more custom workflows and apps are created and shared, it attracts more new customers and encourages existing customers to expand their wallet. All this leads to MNDY having a much higher $100k+ customer count than ASAN.

{kind=link}

{kind=link}

{kind=link}