Updates - Palantir 3Q22

Summary

- In 3Q22, there's a continued slowdown in revenue recognition but an upturn in RPO, deal value, & # of large deals made - positive signs for future revenue.

- Ontology, ontology, ontology – this is Palantir’s fundamental differentiator versus the competition. We recap on its significance.

- The current valuation indicates Palantir will not reaccelerate growth.

- However, the deal value and RPO indicates somewhat of an acceleration in the next few quarters, and we think more growth will come when macro improves.

piranka

Audio Preview:

3Q22 Review & Financial Trends

3Q22 revenue came in slightly higher (+$2.8m) than the guidance, but this was not enough to stop the stock falling below $7/share. There were a few disappointing metrics that we’re sure investors will have honed in on – such as the $0.01 EPS miss, the sharp drop in commercial growth (3Q22 YoY growth of 17% vs 2Q22 YoY growth of 46%), and the continued decline in non-GAAP EBIT margin (3Q22 Adjusted Operating margin of 17% vs 2Q22 of 23% and 3Q21 of 30%). Other negatives were the continued decline in gross margin, and FCF margin that has fallen into the single digits. And while U.S. commercial YoY growth was 53%, it has decelerated sharply, from 136% YoY growth only two quarters ago.

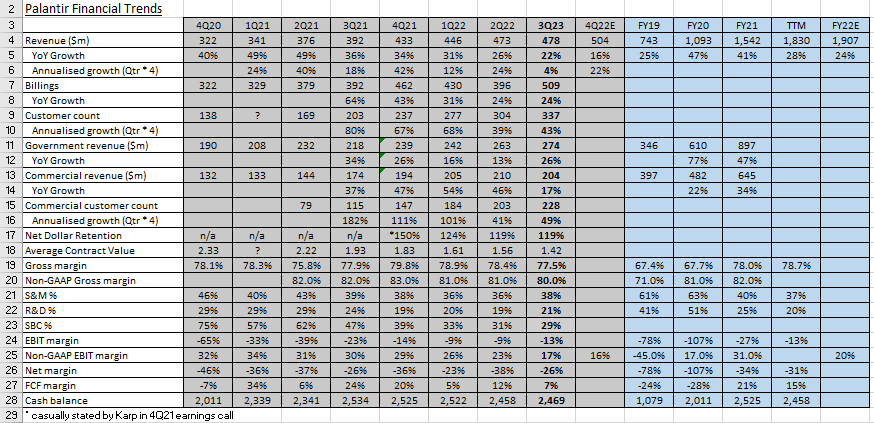

To see the following table better visit this Google Sheet and go to the Financial Trends sheet. There you'll also see the updated valuation - we discuss this in more detail in the Valuation Considerations section.