Themes - SysMoore & Energy (Pt.3.2) Reactor Design & Fuel

Summary

- The U.S. must shift from custom, one-off nuclear plants to industrialized, modular manufacturing of standardized SMRs to meet AI-driven energy demand and compete with China.

- Applying SMR principles to traditional light water reactor designs is the least compelling investor approach, as small scale sacrifices economies of scale without reducing legacy complexity.

- Advanced coolants like sodium, helium, and molten salt offer major advantages over water — including passive safety and higher efficiency — but each carries unresolved engineering challenges.

- Limited HALEU fuel and TRISO fabrication capacity represent critical bottlenecks that will delay nearly all advanced reactor deployments regardless of licensing progress.

- Thorium-fueled molten salt reactors are the theoretical ideal for nuclear energy but remain the furthest from commercial reality.

SMR Vendors

SMR Vendors: The Path to Nuclear Industrialization

If the US intends to build sufficient power generation to close the AI demand gap and compete with China's nuclear buildout, it must develop an efficient and rapid method of reactor production. The most obvious answer is modularization: rather than constructing large, one-off, customized nuclear plants — each a unique megaproject with its own supply chain, regulatory review, and construction learning curve — the industry should move toward standardized designs assembled from pre-fabricated modules on continuous production lines. The goal is to transform nuclear construction from artisanal megaproject engineering into industrialized manufacturing, analogous to the transition from handcrafted automobiles to the Ford Model T, or from bespoke aircraft to the standardized Boeing 737 — where mass production of interchangeable parts enables faster delivery, lower cost, higher reliability, and reduced maintenance burden.

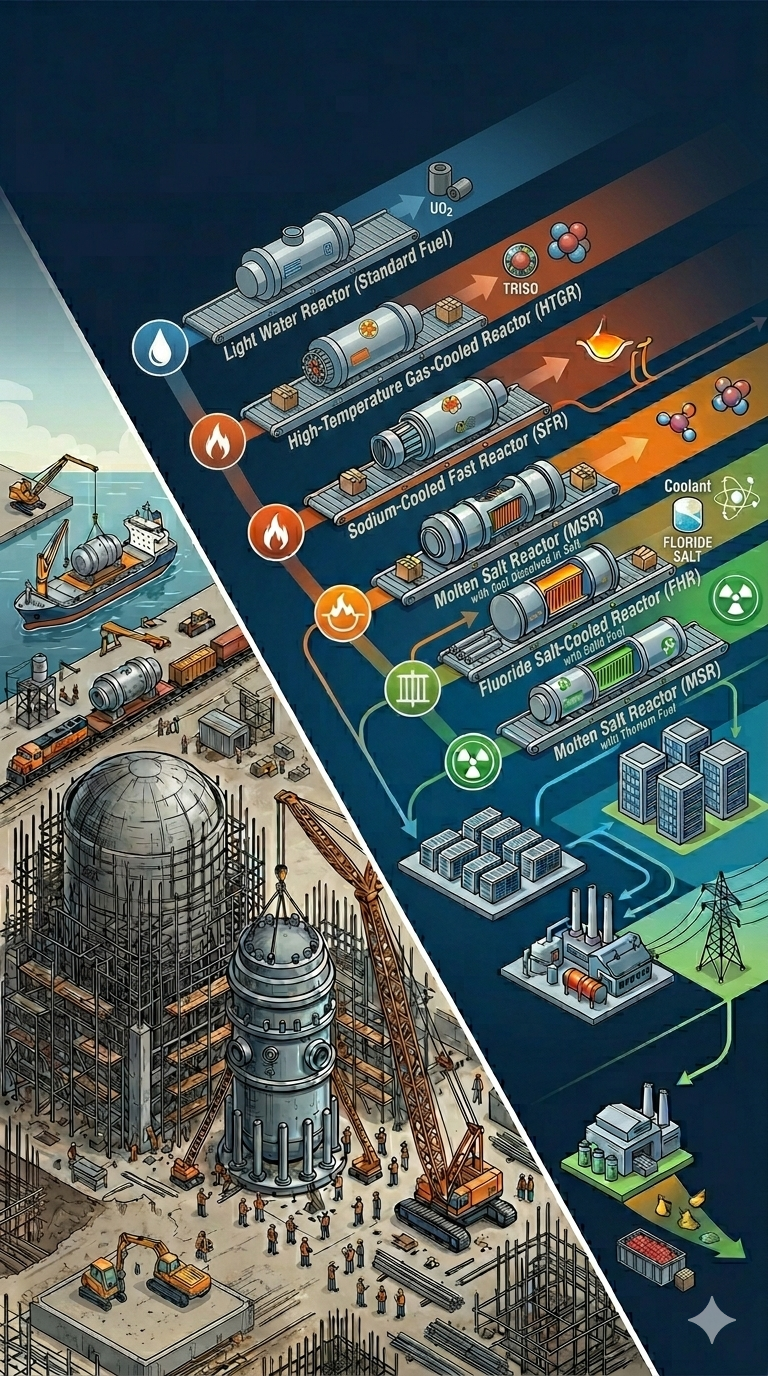

Currently, approximately eleven companies are pursuing distinct SMR designs, six of which are publicly traded. These designs can be categorized along four principal technology routes: Light Water Reactors (LWR), High-Temperature Gas-Cooled Reactors (HTGR), Sodium-Cooled Fast Reactors (SFR), and Molten Salt Reactors (MSR), with an additional category for Fluoride Salt-Cooled High-Temperature Reactors (FHR) that blends elements of HTGR and MSR.

Established nuclear incumbents — Rosatom (Russia), CNNC (China), Rolls-Royce SMR (UK), and GE Vernova-Hitachi (US-Japan) — are pursuing SMR designs based on the familiar light water reactor architecture. These players have deep political relationships, regulatory familiarity, and operational know-how with the existing LWR technology route. Essentially, they are applying the SMR production philosophy to change how reactors are built, but not what is being built.

We believe this is the least compelling approach to SMR for investors, because the economic disadvantages of small scale may outweigh the benefits of modularization when applied to LWR technology. The core issue is that SMRs are, by definition, small. This means they sacrifice the economies of scale inherent in large reactors. When SMR principles are applied to LWR designs, the redundant safety systems, containment structures, instrumentation and control systems, and other fixed-cost components that can be amortized effectively over a 1+ GW plant become proportionally much more expensive when spread across a 50–300 MW unit. The result is that cost per installed kilowatt may actually be higher, not lower, for LWR-based SMRs relative to large reactors.