AVGO + VMW - Value In The Rough - Part 1

What was a surprise to many observers, in May-22, AVGO made a bid for VMW for $61bn - 50% in stock and 50% cash raised via new debts. We'll start by analyzing the rationales behind this bold acquisition and then cover AVGO in more depth in Part 2.

AVGO + VMW has been the strongest backbone of the Software Defined (SD) revolution

The majority of analysts don't cover the history of the SD movement that has brought tons of disruption to incumbents at the start of the 2010s.

Software is eating the world, and to make it work, you need to do it from the infrastructure level.

One clearer and broader SD movement is Software-Defined vehicles whereby TSLA is pushing the total electrification and digitization of autos. The implications are huge, as previously cars were developed integratively and resulted in rigidity. It takes auto makers 5-7 years to bring one car to the market with chips made 10 years ago and the priority is more around stability and safety rather than performance and utility.

What TSLA did is bring the software DevOps mindset to the car industry, and the components are decoupled from another, enabling faster development and greater flexibility. For example, during the peak of the supply chain crisis, TSLA was able to switch to another chip by changing software codes, while traditional automakers like Toyota have had to wait and pay for chips at a 10x higher price because of distributors' concerted price manipulation antics to profit from the crisis.

To understand why SD is such a big deal, first you need to understand the previous world of IT infrastructure. Before the SD movement, IT infrastructure didn't move and evolve as quickly as that of the upper application stack. With the emergence of hyperscalers, and mega apps like Facebook with a billion plus user base, a performant, cost-effective, and agile IT infrastructure was needed. However, existing incumbents are most of the time unwilling to cooperate as the main priority is to defend their castle, juice out nice margins from low growth businesses, and lay back with steady compensations. This is a great opportunity for disruptors to innovate.

VMW in particular, led the revolution of SDDC (Software-Defined Data Centre) that includes building a new abstraction layer around compute, storage, and networking via software plus COTS (Commodity-Off-The-Shelf) hardware.

Take networking for example; previously, an org has to sign a lump sum deal with CSCO for data centre networking and what they get is CSCO’s networking box and pre-built software in it. The hardware box is a blackbox, priced at 2x+ that of the raw material costs. The software is written exclusively for the hardware, with little room for configuration and customization. Furthermore, because the software is tightly coupled with the hardware, it takes 2-3 years for a new generation of hardware to come into the market. Put simply, this old model results in slower to adapt, expensive, and less performant IT infrastructure.

The need for a new ecosystem is so profound that there are various players pushing for SDN (Software Defined Networking). There is META pushing the open SDN standards in collaboration with hardware OEMs. There is Red Hat, now part of IBM, pushing the open source SDN stack. There is VMW, which under the leadership of Pat Gelsinger, acquired Nicera at a hefty premium, and then created NSX for SDN like what ESX is for computing. There is ANET that focuses on buying COTS hardware and then develops its own networking operating system on top.

At a high level, in the age of SD we could divide players into two broad categories - hardware and software. Here the hardware is of less value because it is built via commoditized, generic, off-the-shelf components that anyone can buy, plug in and play with.

SDN makes sure that end customers no longer need to pay the hefty premium for hardware boxes and by standardizing the data plane (hardware & basic layer), vendors can focus on quickly delivering agile, sophisticated, and cost-effective software.

The most important players, however, is not the software developers but the chip makers. When hardware has become commoditized, it is a low margin business to be an OEM like DELL or HPE. To deliver on the promised ROI of SDN, orgs need ASIC accelerators for networking. And buying COTS INTC x86 CPU doesn't help when competing against CSCO's custom silicon. AVGO spotted the opportunity here, risked the front-end costs associated with chip development, ecosystem building, and SDK development, and brought networking ASICs to the market. Albeit, some small competition from Barefoot Networks (acquired by INTC) that makes ASICs, AVGO's initial launch of the trident switch ASIC achieved wild success as it serves as the key to downstream ecosystem players as they compete against CSCO.

With the raw power of AVGO as the central chip provider, and the unleashed innovation from SDN vendors, the combined product is able to beat CSCO both in features and TCO. Although SDN didn't entirely kill off CSCO as the latter then opened up its tight software control somewhat, it did open up a huge field and brought players like VMW to reach product and market share parity with CSCO in data centre networking, all without the need to go into the heavy duty hardware business. Furthermore, with the success of AVGO's ASIC as the de facto standard for various SDN vendors to power their COTS hardware, AVGO gains the economies of scale. It is able to leverage the scale to build the best networking ASIC, rivaling integrative vendors like CSCO. Eventually, vendors like JNPR and CSCO also offered their boxes based on AVGO chip.

Here, we shouldn't underestimate AVGO's ability to sense the revolution that is brewing, seed innovation boldly at the early stage, and collaborate with the best disruptors. Although the company is multi-decade old with revenue in double digits of USD billions, its vibe is very akin to innovative startups. Furthermore, the world of semiconductors has been relatively slow-moving and less sensitive to changes in the upper software stack. We find AVGO's success in SDN to be a strong indicator that the company is not in the same legacy tech cohorts of CSCO or IBM.

Source: Convequity

Fabless is becoming software centric

AVGO's success in SDN via understanding software and co-innovating in the upper stack is not an outlier for the industry. Arguably, the biggest success story of the fabless world in the last decade comes from NVDA who hired more software engineers than a typical pure software shop. The secret weapon? CUDA (Compute Unified Device Architecture) and the related middleware stack that is the de facto standard for scientific simulation and AI/ML training/inferencing.

NVDA spent more than a decade doing heavy duty infrastructure software work to optimize the performance of various accelerated workloads. Then, it makes it super easy for software developers to use and innovate on top of CUDA without the need to worry about complex coding and optimization for parallelizable compute.

This is a huge paradigm shift in the world of chip/fabless that is either missed or not appreciated by generic analysts and public investment community. The next successful fabless firm will very likely be a software one whereby it is not enough to design chips only, but also necessary to understand the changing architecture of software, and develop an optimized infrastructure software stack to end users.

INTC, under the leadership of Pat Gelsinger, is aggressively executing this strategy with massive hiring of software engineers to develop oneAPI that streamlines the SDK and middleware together. Jim Keller's Tenstorrent is a great example whereby the founders spotted the change in demand for software 2.0 and then developed chips with heavy emphasis on a custom optimized compiler to deliver high performance gains with ease of use. We shall expand this topic in another report.

To AVGO, it is the same. To be able to thrive continuously, it needs to keep up with the game, not only with the success of SDN. AVGO's broadband, storage, and other sides of networking, including carrier networking, are also becoming software centric. A comprehensive SDK and standardized/optimized middleware to help software solution providers, or OEMs to develop and finish products quicker at lower costs and higher flexibility, is an absolute killer. QCOM has demonstrated the power of this in its mobile and IoT SoC business.

By acquiring VMW, AVGO will be able to become a leader in infrastructure software space, and keep the most valuable parts of the business in the value chain - software and chips, excluding other commoditized and less sophisticated parts. AVGO's semiconductor accelerator chips combined with VMW as the infrastructure software being an orchestrator could unleash tons of value for end customers. As we've highlighted before, the future of logic chips is going to be DSA in the sense that each domain-specific workload is going to be handled by domain-specific accelerator. This is a promising potential for further performance gains and keeping Moore's Law intact. However, it also requires further software and hardware integration, and a major architectural shift for both hardware and the software.

With VMW as a single entity, VMW could develop specific orchestration optimization functions for AVGO and take on integrated solutions that don't currently have SD components within. VMW + AVGO could provide highly flexible software control plane while the underlying hardware data plane is highly optimized for best TCO. This both deepens AVGO's moat but also opens up a great greenfield for AVGO to further grow its networking, SAN (Storage Area Network), and various accelerator business.

Financially Attractive

The aforementioned two points are the strategic rationales that, in our opinion, are generally unacknowledged by the public. The financial implications are the most obvious points of this acquisition.

According to AVGO, the deal is structured to be:

- VMW shares valued at $61bn plus $8bn in net debt. $61bn would be 50% paid in cash and 50% paid in newly issued AVGO shares. $32bn in new debt financing is secured.

- The combined new entity would be 88% owned by the existing shareholders and 12% owned by VMW shareholders.

- The deal is expected to be closed at the end of FY23, which is Oct 29, 2023, subject to regulatory approval although there are no extraordinary concerns.

- VMW will also be managing the portfolio of CA Technologies and Symantec. AVGO's existing Broadcom Software division - with about $5bn in run rate, 90% in GM, and 70% in EBITDA - will be rebranded under the name of VMware.

- Management is targeting to increase VMW's stand-alone EBITDA to $4.7bn to $8.5bn within 3 years of closing - TTM is currently $2.9bn. The mid-point of that range equates to 50%+ EBITDA margin.

- Long-term target for revenue is recurring revenue growing in the mid-single digits.

- The incremental EBITDA margin gain would primarily come from shared operations, thus eliminating G&A, and partially from the synergy associated with expanding the core strategic accounts from 600 to 1500 that share many characteristics with existing Broadcom Software customers.

- Unlike the notorious yet successful turnaround of Symantec and CA, AVGO plans to continue the investment in S&M to drive more growth, and thus the resultant EBITDA margin is expected to be 5%+ less than the existing Broadcom software .

- The plan is to create the most comprehensive infrastructure + software stack ranging from legacy-yet-still-relevant mainframe (existing Broadcom), bread-and-butter private cloud, emerging Kubernetes and container software, and future hybrid clouds.

- To secure all of these platforms, Symantec will be for legacy systems and Carbon Black & VMW's existing security stack will be for modern infrastructure security.

- Business from VMware and infra software will be 50/50 with the semiconductor business.

- AVGO will be the biggest supplier of IT infrastructure software.

On to valuation considerations; the EV is at $58bn while the TTM EBITDA is at $2.9bn, which means that the EV/EBITDA is at 20x. AVGO's non-GAAP measure of TTM EBITDA is $4.7bn that equates to a 12x EV/EBITDA. The 12x would be in the low-side of normal range for a 30%+ EBITDA margin and low teens growth company, while the 20x is slightly above the normal range. Given the current downturn, this is not a value bargain for AVGO. This is probably the reason why both Dell and Silver Lake (majority shareholder of VMW) voted unanimously for the deal and there was no subsequent additional bidder. If AVGO is able to achieve the $8.5bn EBITDA target then it is valued at 6.8x, which would then make the deal seem much sweeter when compared to most PE deals, especially considering the quality of assets and the expected easier execution.

As shown in the next slides, AVGO's analysis over VMW's fundamentals is spot on and aligned with our own views.

- Private cloud is here to stay for a variety of reasons including security, data-related compliance, customizations, and cost predictability.

- Public cloud is growing faster, but hybrid and multi-cloud configurations will be increasingly needed.

- VMW's private cloud stack is comprehensive and category leading across compute, network, and storage virtualization.

- VMW's infrastructure automation is able to connect the private and public cloud stacks together.

- VMW's public cloud stack is a new orchestration layer for multiple cloud IaaS, which is in strong demand by the large enterprises that AVGO's software division is targeting.

Hidden Optionality?

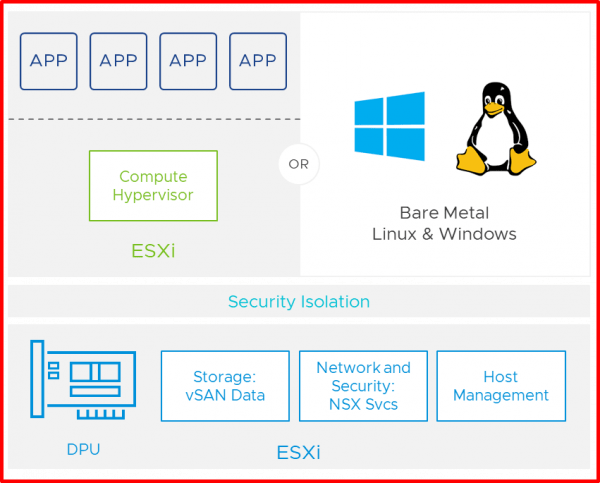

In AVGO's core domain of networking, NVDA is trying to disrupt via DOCA (Data Centre On a Chip Architecture). Although it is more related to HPC (High-Performance Compute) and AI/ML use cases, DOCA and DPU (Data Processing Unit) are becoming a bigger theme across the industry.

The emergence of DPU comes from the need to squeeze more efficiency gains from hyperscalers and those running massive cloud infrastructures via DSA (Domain Specific Accellerator). Previously, infrastructure related workloads such as networking, security, protocol, and virtualization were all running on the CPU. Therefore, there has been a great opportunity for chip makers to create DSA chips to offload and accelerate these infrastructure-related workloads to the DPU and allow the CPU to work 100% for client workloads.

This means that hypervisors and infrastructure software will be moving to run on DPU. Unlike generic CPUs, DPUs will require specific optimization, and thus tighter software + hardware optimization. NVDA is trying to replay its CUDA playbook here, and it created the new DOCA architecture to help orchestrate DPUs and make it easier for software developers/engineers to build applications on them.

VMW is also starting its Project Monterey to develop a new version of VMW software running directly on DPUs.

Thus, if AVGO is able to collaborate with VMW on DPU again, it could be another strong synergy that could further supercharge its growth and eat the market share of generic CPU players who don't own DSA IPs and the software stack. As all the public focus on the deal appears to be around the AVGO ASIC and VMW SDDC synergies, we view this DPU opportunity as a major bonus, and something that gives AVGO some optionality when it comes to developing its growth outlook.

AVGO's Track Record & Shareholder Returns

AVGO has proven record of cutting costs aggressively while maintaining a certain level of growth. For years, Hock Tan has been meticulously choosing M&A targets, raising finance, and then paying down the debt via growth and cost-cutting schemes.

Furthermore, AVGO is smart at playing the capital structure. It is able to finance most of the transaction with a safe level of leverage and small percentage of dilution. Unlike many other M&A-heavy tech giants, AVGO is able to deliver long-term compounded shareholder returns amid small dilutions from M&A.

AVGO's pro forma debt to EBITDA ratio is at 2.5x, with weighted-average debt duration at 10.2 years, and short-term debt at $392m. This is a very smart company not only in tech fundamentals but also in financial engineering to deliver higher shareholder returns.

Relative Valuation

Most of the TTM and forward valuation metrics are either below or equal to the current sector median, or below or equal to AVGO's 5-year averages. For a well-managed, stable semiconductor company growing at c.20% with 35%+ operating margin, we think this presents investors with a good investment opportunity.

We view AVGO as a steady-returning stock for those looking for lower volatility, attractive return, and relatively lower risk in a retirement portfolio, for example. AVGO's unique buy-and-hold acquisitive strategy with capital from cash generative businesses is very similar to PANW, and BERK more broadly speaking. We shall dive further into AVGO, its semiconductor business, and its unique capital structure in the next report.