Convequity MSU: Meta Platforms - Jan 2023

Summary

- After META's surge over the past 1 year, the stock isn't super cheap, though on a conservative projection basis, there seems to be 30%+ upside left.

- In this MSU report, we've found that M views are extremely shallow with limited alpha, and S views are overly short-term focused.

- In the U part of MSU, we aim to provide a deeper view META's ads business, its AI endeavours, and the metaverse prospects.

As a reminder, here are the MSU scoring options. M, S, and U will be given one of the following scores:

+++, ++, + , /, -, --, ---

For META, we make the following scores to compare and distinguish the three types of views:

M+, S++, U+++

Here is a 9-point summary of where the M, S, and U viewpoints differ on META:

- Generally, U has a richer fundamental view with a longer-term perspective than both M and S.

- M sees growth decelerating to high-single digits in 3 years, while S and U expect double-digit growth to continue.

- S focuses on META's AI that is already established as revenue generators, while U analyzes the prospects of future AI initiatives unveiled at Meta Connect 2023.

- U provides more in-depth analysis of AI innovations like Llama and I-JEPA, which is absent across M and S circles.

- U sees open-source LLM strategy as a competitive advantage while S acknowledges but does not emphasize it.

- U expects Advantage+ Campaigns to take market share from Google Ads which M and S don't analyze.

- U has a deeper understanding of the resurgent ads growth for META, which doesn't appear to be discussed in M and S communities.

- U provides more granular competitive analysis versus ByteDance, which M and S do not touch upon.

- U sees the metaverse as an underappreciated long-term growth driver versus M and S.

Now we'll dive into M, S, and U in more detail. The U section is extensive. For an even deeper dive, be sure to check out our three-part META deep dive released in 2022, much of which is still relevant and useful today.

M

- Generally, META's scope seems too big for the typical retail-oriented investor to analyze. If you take a look on Seeking Alpha, most of the META coverage is simply repeating Zuckerberg's commentary from the 3Q23 earnings call and the Meta Connect 2023 in October. Other Seeking Alpha authors have not even bothered to do that, and merely comment on the past year of efficiency and how there is still room for more efficiency in the coming year.

- Some Seeking Alpha articles do discuss META's prospects in AI, but they are only paraphrasing Zuckerberg's Meta Connect 2023 comments. As we share in the U section, a deeper understanding of META's progress in the open-source LLM world will help investors understand the core of META's GenAI competitive advantages.

- On the whole, M appears to be moderately bullish on META's prospects for infusing more and better AI into their platforms to increase user engagement. Furthermore, Advantage+ Campaigns (ASC) seem to have struck a chord with M, following Zuckerberg's comments in the 3Q23 call about reaching a $10bn run rate.

- The bullishness comes from extrapolating the LTM through to the NTM. However, we surmise that META's resurgent growth has largely come from Chinese ecommerce players' ads campaigns, and whether this continues is uncertain. This is something not discussed across the numerous retail-oriented META reports we've read, but is something we dive into in the U section.

- The prospects of the metaverse is not deeply discussed within M circles, but more so than S. Even for retail or the broader market, the realization of the metaverse seems too far away to be factored into a META thesis.

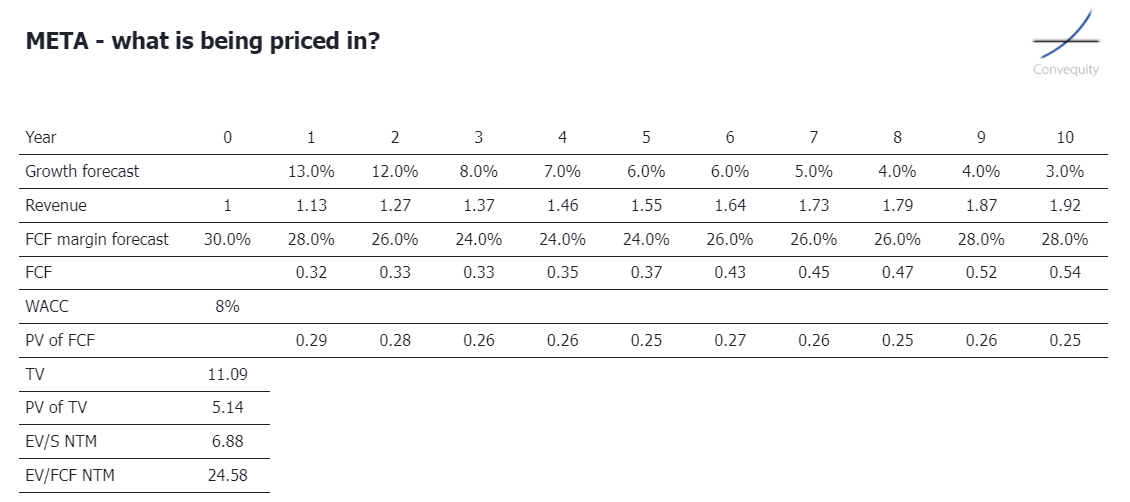

- Currently, the actual EV/S NTM is 6.5x and we calculate the EV/FCF NTM to be 25x. By playing around with the shortcut DCF-to-Multiple model shown below to make the forward growth and FCFs equate to these multiples, it looks as though the market is pricing in a decline in growth to high-single-digits in only 3 years from now, along with a near-term dip in FCF margin (due to the heavy capex requirements for both AI and the metaverse) which doesn't return to the elite level of 30% by the terminal stage. There are a number of different ways to tweak this model, though it seems as though what is being priced in right now offers substantial upside for the bulls who are vocal across retail investment channels.

S

- The few Wall Street reports we have seen, as per usual, focus on the short-term catalysts, such as the increased engagement across apps attributed to the AI-based discovery engine, the growing Reels monetization, and the rapid growth in Click-to-Messenger ads. There is also a fair amount of discussion on META's Advantage+ Campaigns (aka ASC) that have had a big impact on the ROAS (return on ad spend) for advertisers.

- In addition, there is some consideration as to META's progress in open-source LLMs and MLLMs (Multimodal LLM), though generally this does not seem to be a hot talking point, most likely because there is no immediate monetization on the horizon. However, over the long-term, as we elaborate on in the U section, the open-source LLM endeavours could prove to be a significant moat enhancer for META as we delve deeper into the world of GenAI and eventually AGI.

- Generally, the short-term thesis for S appears to be META maintaining double-digit growth while squeezing out further operating efficiency gains, emanating from continued high user engagement levels, the recently launched ASC, and a slower hiring trend.

U

We view META's business as having the cash cow (ads business), the short-term growth catalyst (AI), and the long-term growth catalyst (metaverse). We will breakdown the U section in accordance to this categorization of META's business. Though, firstly, we'll touch on META's financials.

Financials

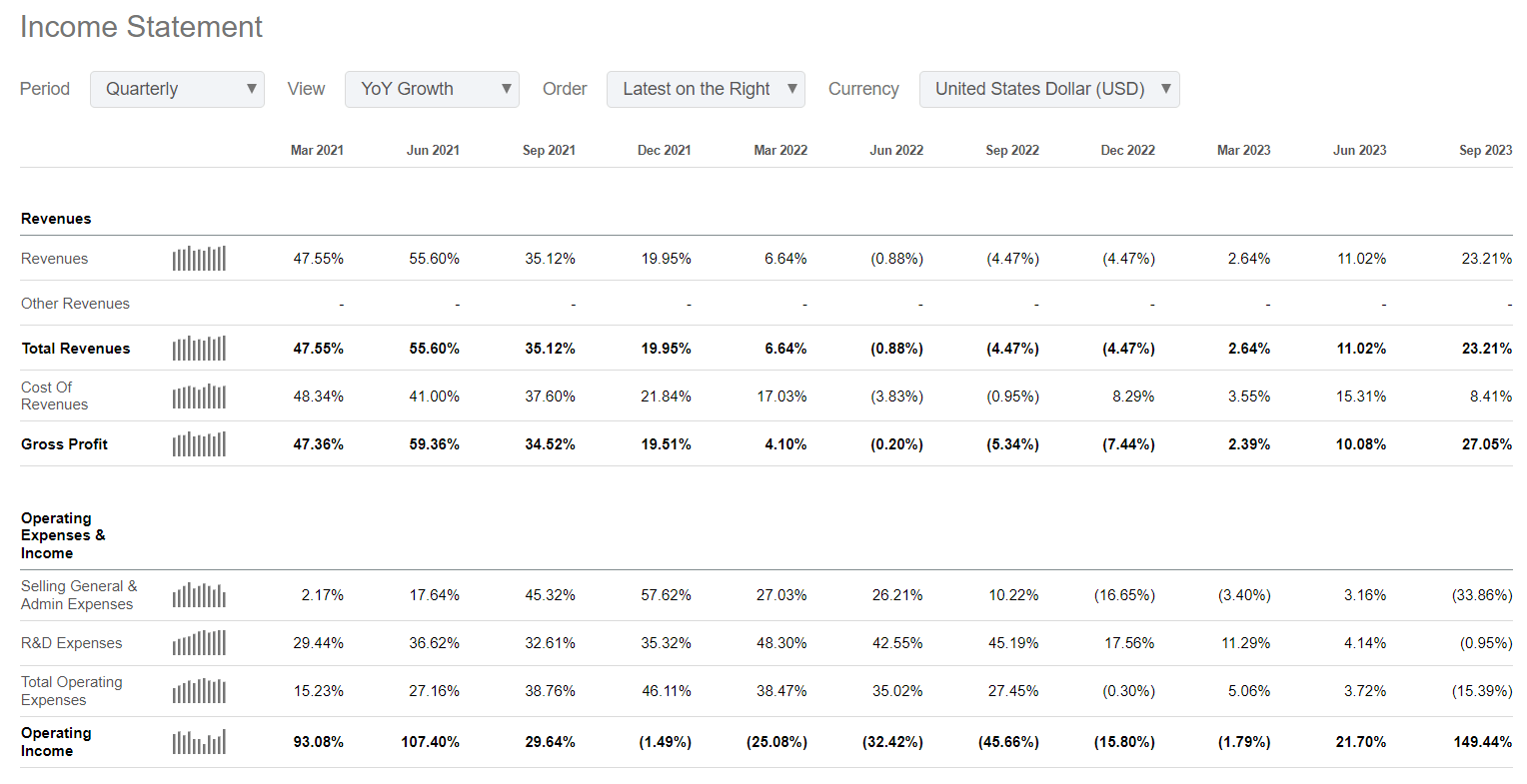

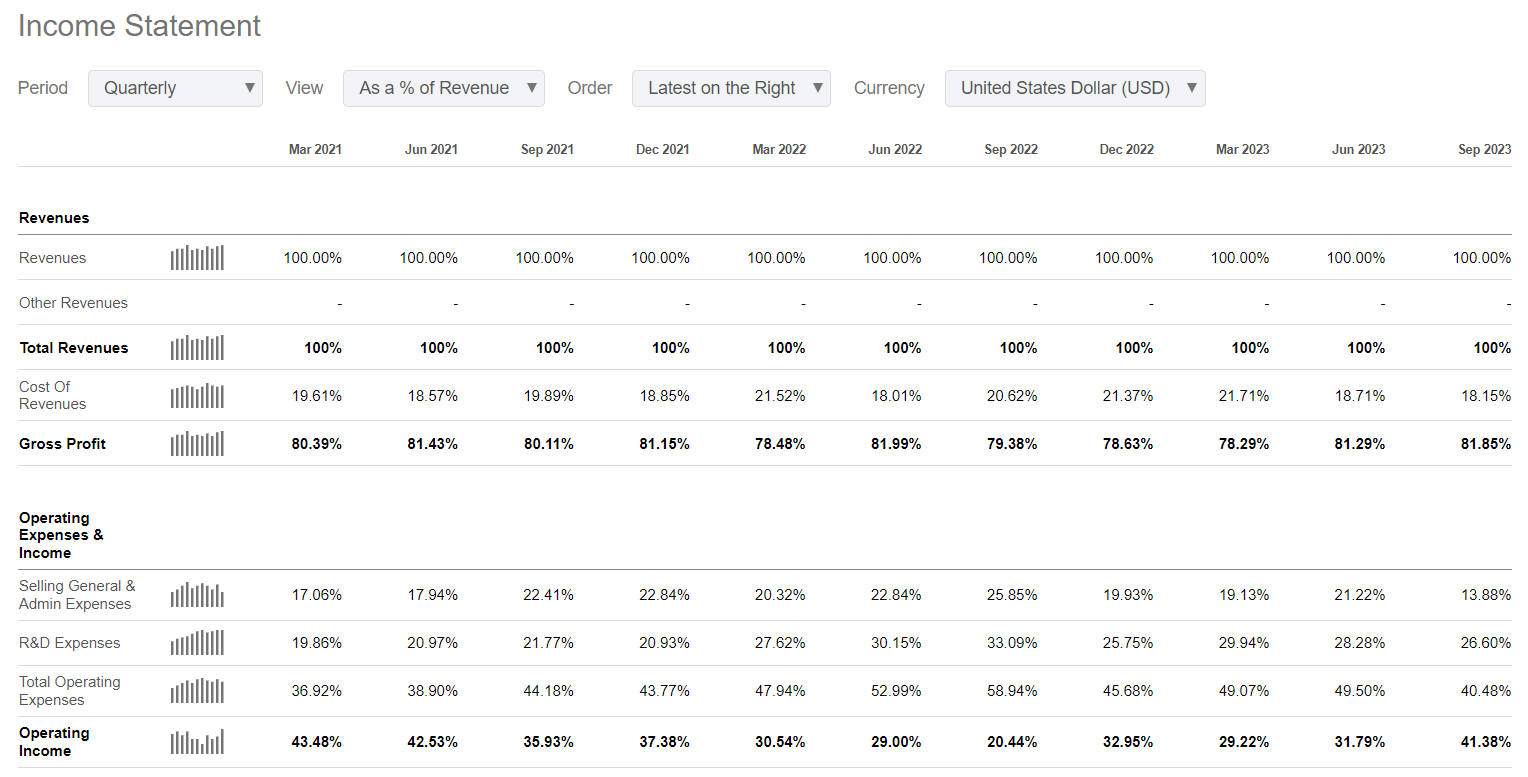

- The improvement in META's income statement financials is obvious for all to see - META has achieved a reacceleration of growth while cutting costs. What is not so apparent is the ramp up in productivity. For FY22, META's LTM revenue per employee was $1.35m, and in 3Q23 its TTM revenue per employee is $1.92m. This is a 42% increase in productivity in just nine months, and to us, is a more impressive metric than what can be gleaned from the income statement alone. With more AI usage, internally and externally, one would expect the rev/emp to continue rising. The prospect of an integrated platform across the Internet and the metaverse could be another lever for higher productivity.

Ads

- META’s Advantage+ Shopping Campaigns, or ASC, is a revolutionary milestone in its ads business, albeit not pervasively discussed among the investor community, and is the first enhanced optimization model since META faced the headwinds emanating from iOS 14.5, released in April 2021. ASC streamlines the ad creation process for advertisers, providing an automated and more efficient and targeted approach to reaching consumers. Historically, META’s ads campaigns have been good at capturing the attention of no/low-intent buyers with interruption advertising, but have not been highly effective in identifying high-intent buyers. ASC enables advertisers to target both no/low and high-intent buyers, making META potentially more attractive for advertisers that to date use GOOGL’s ads to connect with the latter type of consumer behavior.

- Comparing ASC to GOOGL's search-based ad business, we see a distinct approach to targeting high-intent buyers. GOOGL also offers display ads for interruption advertising on websites to capture no/low intent interest, though the majority of revenue comes from ads that cater to users actively searching for specific products or services, capitalizing on immediate purchase intent. In contrast, META's ASC aims to identify high-intent buyers through AI-driven insights, potentially reaching users earlier in the buying process or those not actively searching but likely to be interested in the product. In 2023, ASC campaigns showed a 160% higher return on ad spend than standard shopping campaigns on META, with a relatively stable cost per thousand impressions (CPM). And this greater advert effectiveness for businesses is flowing through to META’s top-line, as Zuckerberg in the 3Q23 ER call mentioned that ASC has reached a $10bn run rate. These results highlight the efficiency and effectiveness of the ASC tool in driving sales and conversions.