Upstart - Pioneering AI Credit Underwriting (Pt.2)

Summary

- Upstart’s model improvements post-Model 18 have unlocked broader bank approvals and lowered default rates.

- Conversion rates have nearly doubled in five quarters, validating model efficiency and product-market fit.

- Upstart’s improved outcomes have enabled it to negotiate higher take rates, supporting better unit economics.

- Real-time automation is reducing CAC and enabling margin expansion as volume scales.

- Despite negative FCF, a 10.9x EV/GP and DCF-supported upside suggest valuation is attractive for long-term investors.

How has Upstart's Edge Translated into Real Business Performance?

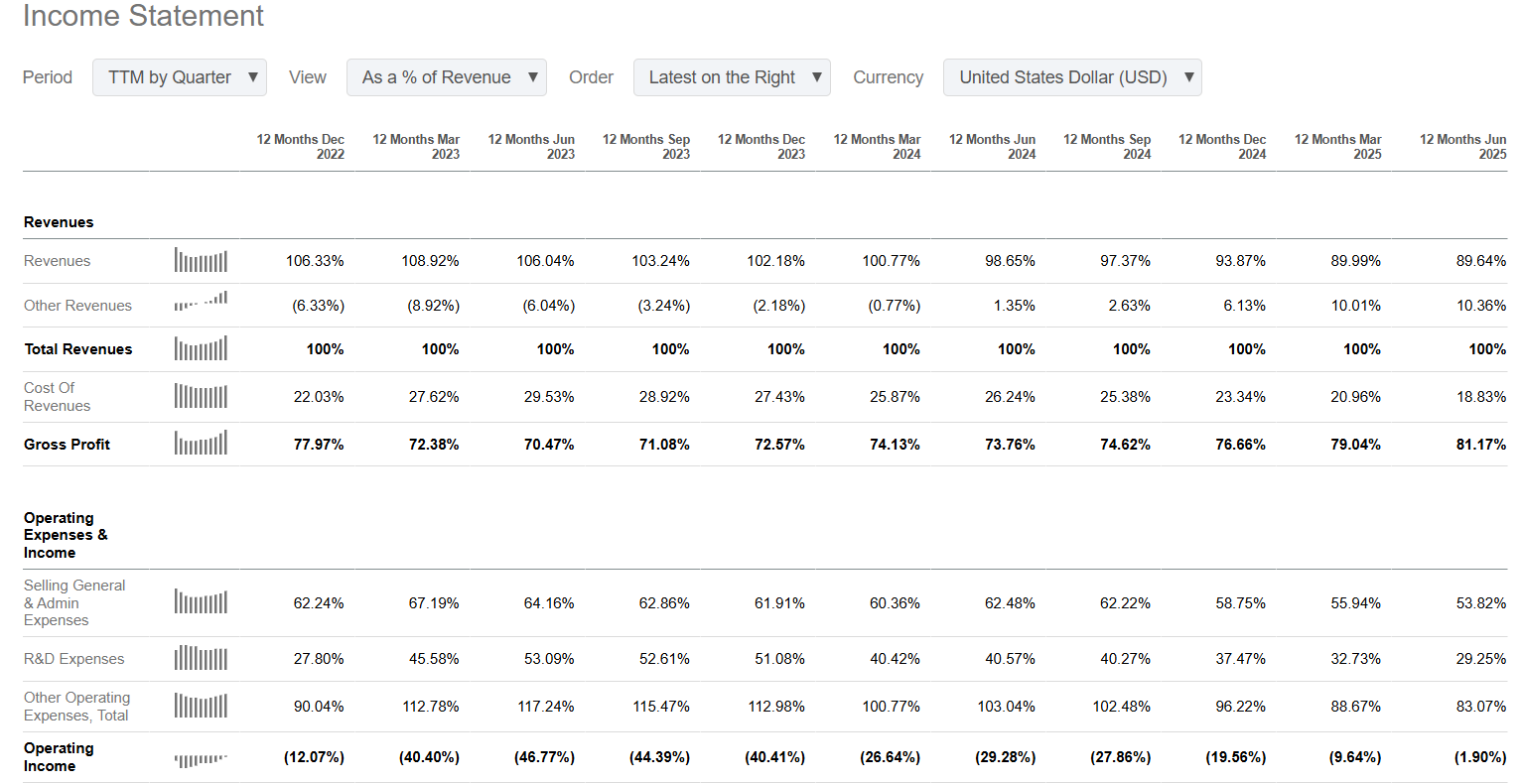

The turning point in Upstart’s financial performance coincides almost perfectly with the release of Model 18 in August 2024. For three quarters leading into 3Q24, TTM operating margins hovered in the negative high-20s, with even deeper losses in the prior year. Then, just as Model 18 introduced APR as an input, PTM, and embeddings, margins began a sharp climb upward. While it’s impossible to assign causality with certainty, the logic is straightforward: more accurate underwriting translates into more approvals for safe borrowers, lower loss rates for lenders, stronger economics for ABS buyers, and ultimately richer profitability for Upstart.

Source: Seeking Alpha

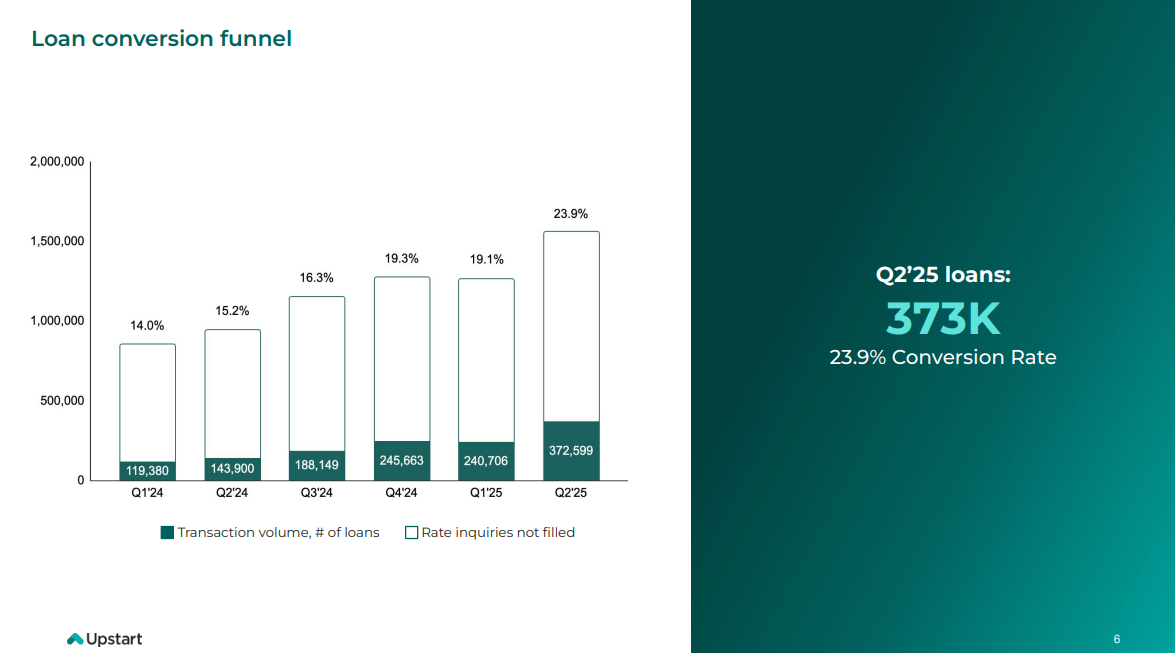

The funnel data reinforces this story. In Q1’24, only 14% of borrower inquiries converted into funded loans. By Q2’25, the conversion rate had surged to nearly 24%, a dramatic efficiency gain in just five quarters. As a result, Upstart’s ML models approve ~44% more borrowers than legacy models while keeping loss rates lower — a dynamic that not only expands financial inclusion but also helps banks capture more revenue from segments previously dismissed.

The jump in loan conversions isn’t just more loans — it’s more good loans. Model 18’s innovations enabled Upstart to separate risk more finely, so banks could confidently fund more of the demand that comes their way. This is the flywheel in action: better models >>> higher approvals without proportionally higher risk >>> more loans funded >>> more revenue for UPST >>> stronger data feedback into the model.

Source: Upstart investor relations

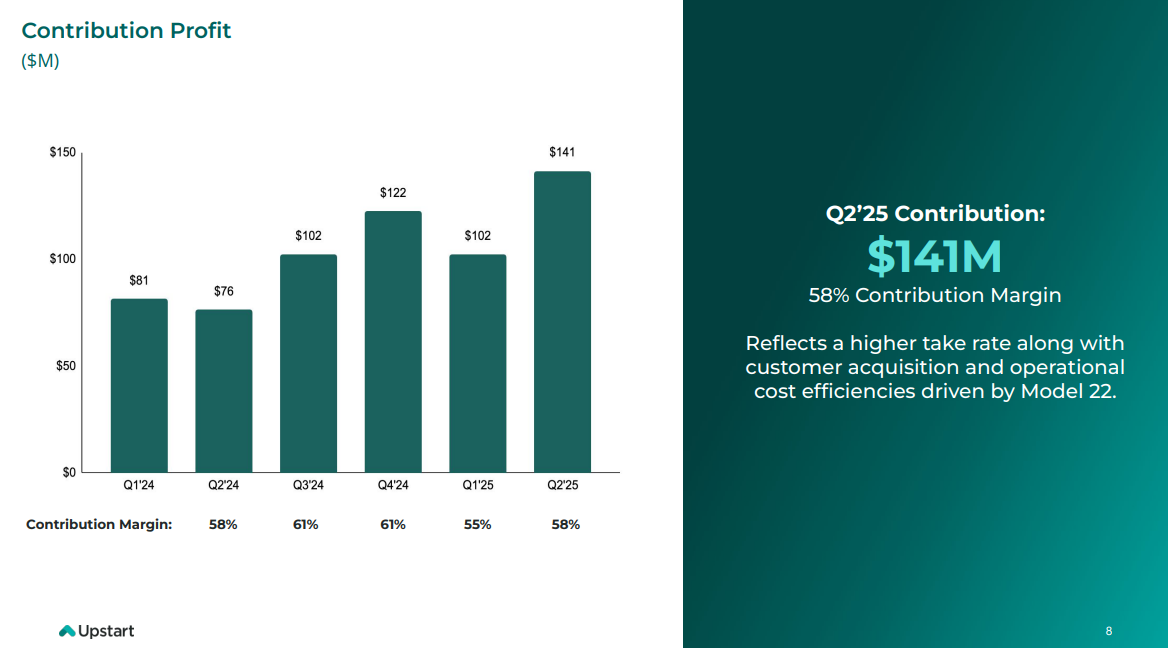

Contribution profit is where these dynamics show up most clearly. Q2’25 saw contribution profit hit $141m, up meaningfully from $102m in Q1’25, with margins steady at 58%. The lift isn’t just from volume; it reflects an improved take rate negotiated with banks. Because Upstart’s models now deliver visibly better performance and funnel conversion, banks and investors are capturing stronger returns on their side. That credibility gives Upstart leverage in contract renewals, allowing them to secure a larger share of the unit economics. The translation of “smarter models” into “higher take rates” is one of the clearest signs of durable competitive advantage.

Source: Upstart investor relations

Automation is another driver. In Q2’25, 92% of loans were fully automated with no human intervention, compared to ~70% just a few years ago. Each point of automation not only speeds up approvals for consumers but also reduces the cost of acquisition and servicing for Upstart and its partners. The breakdown shows the scale effect: automatically approved applications convert at over three times the rate of manually reviewed ones. For banks, this means lower operational drag and faster time-to-loan. For Upstart, it means higher margins at scale. Together, it underscores the power of an AI-native credit platform: efficiency improves with volume rather than deteriorates, which is the opposite of most manual-heavy lending models.