Updates: Palo Alto Networks -From Platformization To AI-Native Security & Observability (Pt.1)

Summary

- PANW is well positioned for AI but still not treated as an “AI winner,” echoing broader concerns that incumbent SaaS platforms will be disrupted by AI-native challengers.

- 1Q26 shows platformization moving from slogan to reality: bigger, longer, multi-product and cross-platform deals, fatter back-end-loaded RPO, and NGS ARR nearing $6bn with a credible path to $20bn by FY30.

- The CyberArk acquisition positions PANW at the identity choke point for agentic AI, giving it the primitives to govern human and machine privileges and to contain agent-driven attacks.

- Chronosphere adds a modern, Kubernetes-centric observability and data-pipelining layer so PANW can pair security with utility which could be a serious growth driver going forward.

- The core upside thesis is that if Arora can prove this integrated fabric both secures and enables AI and agentic workloads in production, PANW’s current “serial acquirer” discount could flip into a meaningful AI rerating.

Executive Summary

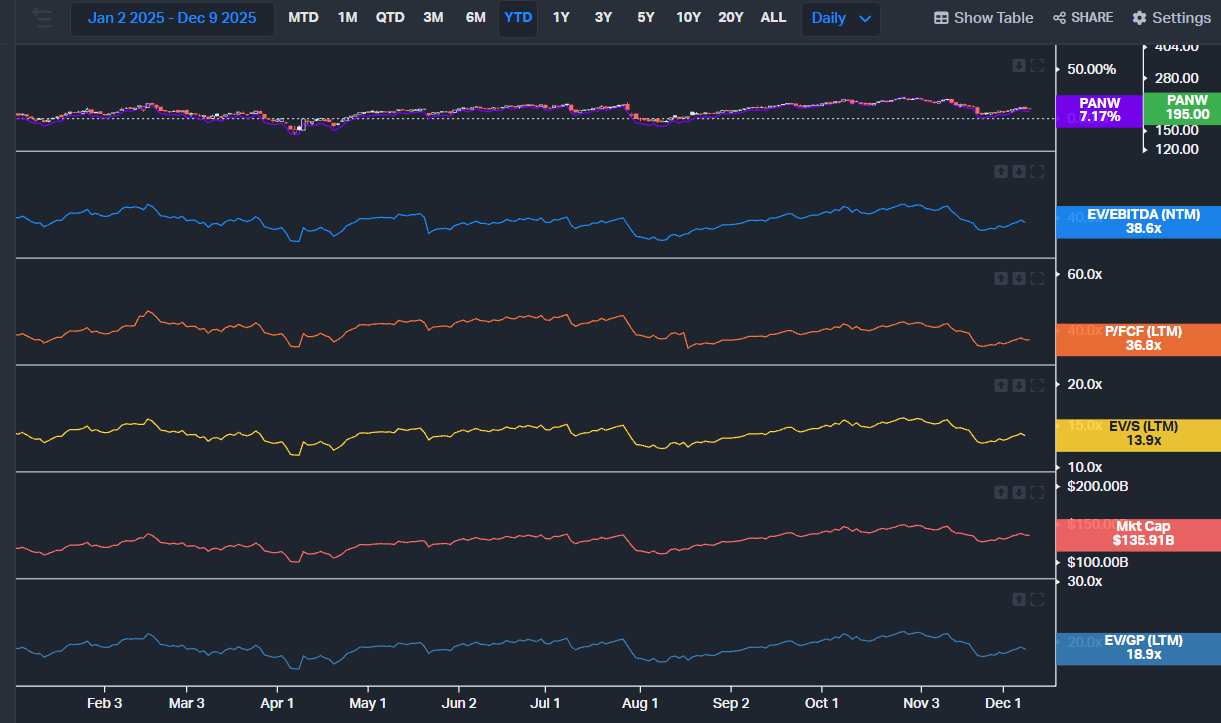

Palo Alto Networks is in a strange place for a company that is, arguably, setting the agenda for what AI-era cybersecurity will look like. As we’ve discussed in earlier work on SaaS more broadly, the market seems wary that many incumbent software platforms could be disrupted or disintermediated by AI-native challengers with sleeker interfaces and better unit economics (early signals like Payback Period have already hinted at this). PANW appears to be caught in a similar perception gap. Strategically, it has one of the clearest roadmaps in the sector: move customers from fragmented point products to three broad platforms — network security (Strata), cloud security (Prisma), and SecOps (Cortex/XSIAM) — and use those platforms as the control plane for users, workloads, and now AI agents. Yet in the market, the stock has not participated in the AI rerating enjoyed by names like SNOW and PLTR. Year-to-date the shares are up only around 7%, a muted outcome in the context of the broader AI trade, with sentiment capped by concern over the sheer size and integration risk of the pending CyberArk acquisition; even Arora’s move in 1Q26 to lift the FY30 NGS ARR target from $15bn to $20bn has not been enough to unlock a sustained rerating. Instead, while PANW still isn’t cheap, the stock is beginning to trade like it has the baggage of a serial acquirer: investors are increasingly asking whether the platformization story is genuinely compounding or simply masking a dependency on ever-larger M&A.

Source: Koyfin

At the core of Arora’s strategy is a simple idea: a platform is not a catalogue of products, it is an account strategy. Platformization, in PANW’s usage, is about getting a single customer to standardise on an entire platform rather than cherry-picking one or two modules. In network security, that means consolidating disparate firewalls and point appliances onto Strata. In cloud, it means treating Prisma Cloud (now renamed Cortex Cloud) as the default control plane for containers, serverless, VMs, and code-to-cloud security rather than buying CSPM from one vendor and CWPP from another. In SecOps, it means building the SOC around Cortex and XSIAM instead of stitching together SIEM, SOAR, and XDR from multiple suppliers. The next stage, which is only just beginning to show up in deal structures, is cross-platform consolidation: large enterprises that are not just “all in” on one platform, but increasingly running two or even all three, so that identity, telemetry, and enforcement policies can be reused across user, cloud, and SOC domains.

The recent acquisition spree sits squarely in this context. CyberArk gives PANW a high-assurance identity and PAM backbone just as AI agents are starting to act autonomously across infrastructure. Protect AI plugs a gap in securing AI pipelines, models, and data. Chronosphere brings a modern observability and data-pipelining layer for high-volume, Kubernetes-heavy environments, building on M3 and Fluent Bit to make large-scale telemetry economically manageable. None of these assets are perfect, and all bring integration work. But they are rare, well-positioned franchises in markets where there simply are not many credible, clean-slate alternatives left. The strategic bet is that identity, observability, and AI security can be combined and integrated into PANW’s ecosystem to generate richer, more contextualised signals — not just to stop attacks, but to keep AI-heavy applications running properly in production.

That is where the line between “security” and “utility” starts to blur. Historically, security was something enterprises bolted on after the fact; applications could still launch and generate revenue even if the security story was thin. In an AI world, that flips. You cannot safely put powerful, tool-using agents into production without strong identity controls, deep observability, and guardrails around models and data. If PANW can show that CyberArk + Protect AI + Chronosphere + Prisma + XSIAM form a governance and control layer that not only blocks bad behaviour but also helps customers deploy, operate, and tune AI systems with confidence — closer to how investors think about PLTR’s AIP as an enabler, not just a shield — the upside to the story changes. It becomes easier to justify AI budgets when the same platform shortens MTTR, protects revenue by keeping services up, and makes AI rollouts viable in the first place.

This is where the investor debate polarises. One camp sees rising complexity, higher execution risk, and the danger that PANW becomes an unwieldy collection of semi-integrated tools. The other sees a company moving early to assemble the minimum viable stack for the agentic era: platforms that already anchor large accounts, now extended with identity, observability, and AI-specific controls that can double as AI enablement. Our bias is toward the latter view, with an important caveat: PANW still needs to prove it can tell and execute a clear “AI utility” story, not just a consolidation story. The share price today embeds a healthy scepticism about M&A and gives limited credit for the AI positioning. If Arora and team can demonstrate that platformization is deepening rather than stalling — bigger, longer, more multi-platform deals; SOCs standardising on XSIAM; secure browsers and identity controls becoming default gating points for both humans and agents — and also convince investors that this stack is a practical way to run AI in production, not just to secure it, then the last year’s underperformance could mark an inflection point rather than the start of structural derating.