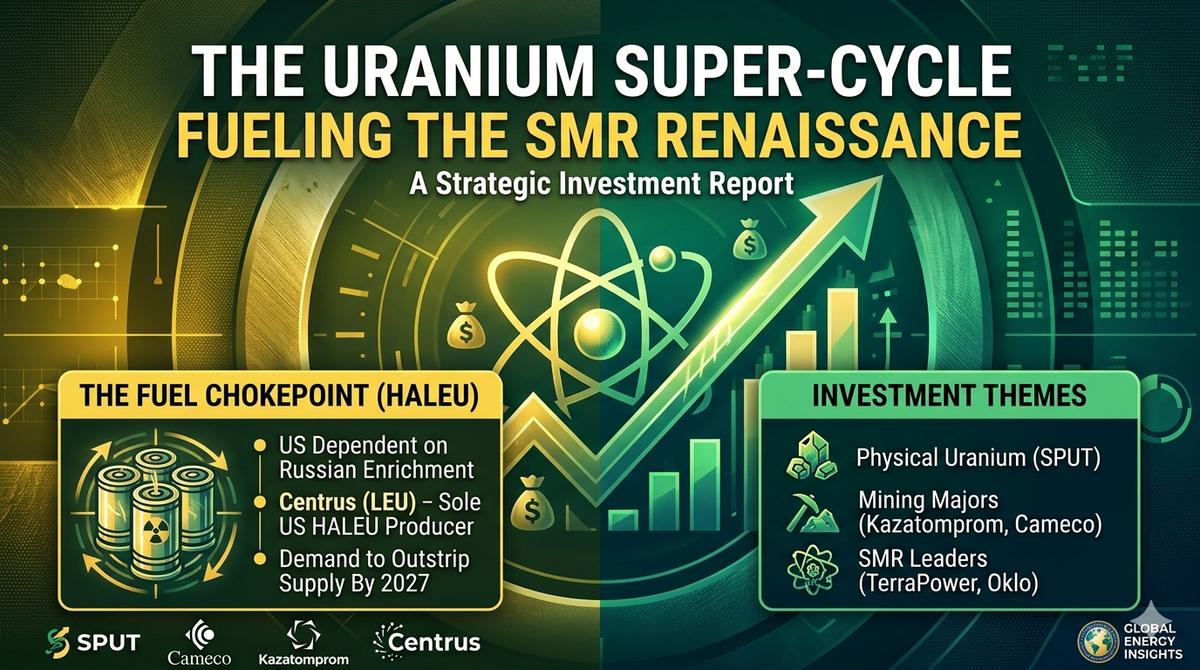

Themes: SysMoore & Energy (Pt.3.3) - The Nuclear Investment Thesis

Summary

- The Uranium Supply-Demand Gap: A three-decade "nuclear winter" of underinvestment has left the global uranium mining industry with a hollowed-out supply base that cannot quickly respond to the current surge in demand.

- HALEU as the Critical Bottleneck: The transition to next-generation Small Modular Reactors (SMRs) is constrained by a severe shortage of High-Assay Low-Enriched Uranium, creating a strategic "chokepoint" that favors domestic enrichment leaders like Centrus.

- Technological Winners and Losers: Sodium-cooled Fast Reactors (SFR) currently offer the best balance of safety and fuel efficiency, while legacy light-water SMR designs like NuScale have struggled to deliver on their promises of speed and cost reduction.

- Silicon Valley vs. State-Led Models: The "nuclear battery" approach led by startups like Oklo provides a faster, simpler deployment model for AI data centers, though China maintains a commanding lead in long-term materials science for molten salt reactors.

- The Structural Bull Case: Uranium represents the highest-visibility, lowest-risk play in the sector because all emerging reactor designs—regardless of which vendor wins—depend on a fragile and geographically concentrated fuel supply chain.

Investing Potential

Having covered Parts 1 and 2, the investment thesis for each publicly traded startup should now be clearer.

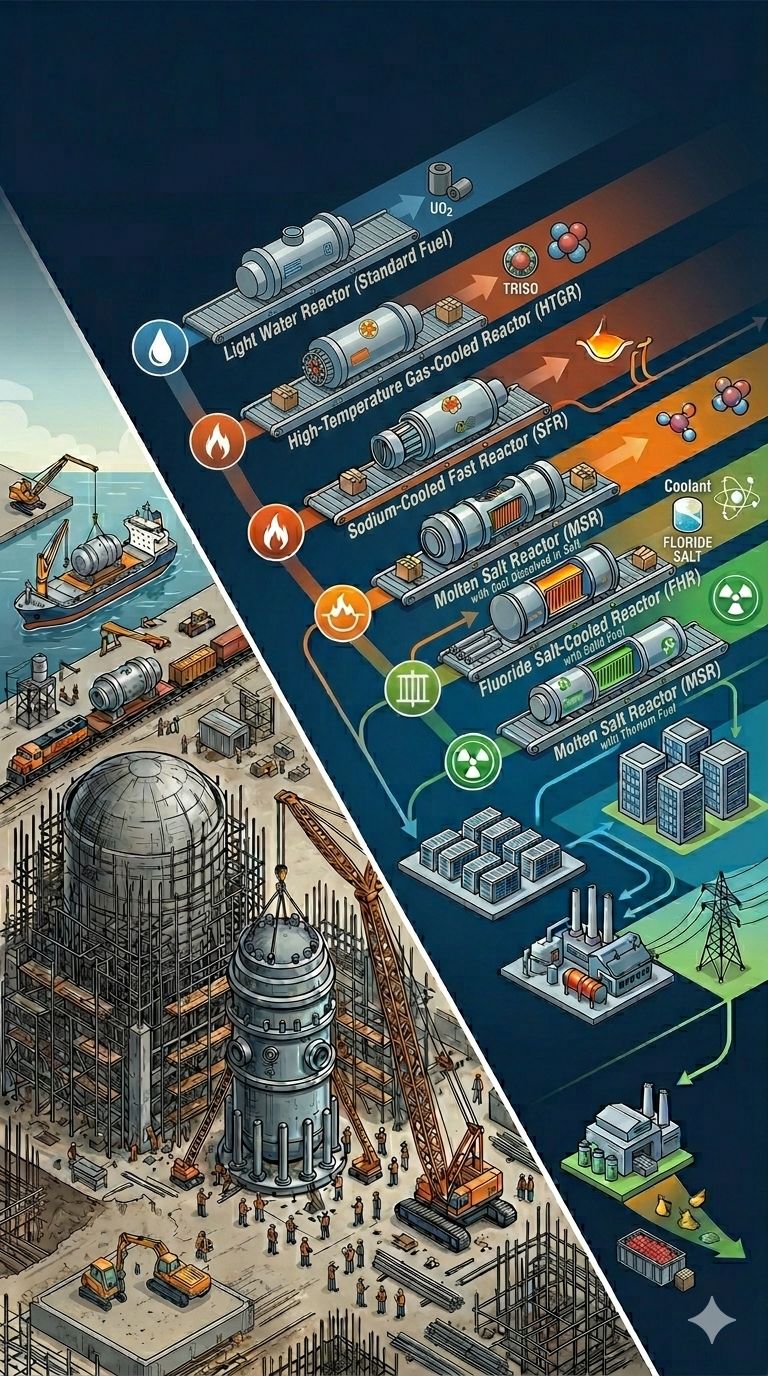

NuScale

NuScale (ticker is SMR) appears to be the weakest SMR player by multiple measures. Despite being founded in 2007, receiving the first — and still only — NRC design certification for an SMR in the US (in 2023), and pursuing the most mature technology route (light water), NuScale has yet to bring a single operating reactor to completion. Its flagship project, the Carbon Free Power Project with Utah Associated Municipal Power Systems, was cancelled in November 2023 after cost escalation pushed the estimated price per MWh from $58 to $89, eroding the project's economic rationale. Nor has NuScale demonstrated the agility expected of a startup; it compares unfavourably to SMR initiatives led by established incumbents with deeper pockets and existing nuclear operational experience.

More fundamentally, NuScale's trajectory raises the most important question confronting the entire SMR concept: can modular construction actually deliver on its core promises of faster deployment, lower cost, and reduced risk of overruns? Based on NuScale's experience, the provisional answer is discouraging.

A corroborating data point comes from China. CNNC — arguably the world's most capable organisation for cost-effective nuclear construction — is building the country's first SMR, the ACP100 "Linglong One." The reactor began cold functional testing in late 2025 and is expected to reach commercial operation in 2026, putting its total construction timeline at roughly five years. That is about how long China takes to build a full-sized conventional reactor. In other words, even the most efficient builder in the world has so far failed to extract a meaningful speed advantage from the smaller modular format. For AI data centre operators, who represent one of the key demand drivers behind the current wave of nuclear investment and who need new power capacity on far shorter timescales, a five-year build is simply too slow.

X-energy

X-energy's HTGR (the Xe-100) occupies an awkward middle ground. It represents a genuine step beyond light water reactors, offering high-temperature industrial heat capability and superior inherent safety through TRISO fuel — but it is not a revolutionary breakthrough. HTGRs lack the fuel breeding and waste-burning capabilities of fast-spectrum designs, and X-energy remains years from actual production.

On the performance metrics that matter most for nuclear economics — fuel utilisation, waste management, and coolant safety — sodium-cooled fast reactors are superior to HTGRs in essentially all dimensions. SFR technology also has a substantially longer operational track record: Russia has operated sodium-cooled fast reactors commercially for years, and the US ran EBR-II as a successful test reactor for three decades. Both technologies are relatively new to US commercial deployment, but SFR is the more proven of the two.