Palantir Q1 2026 - What Cursor Proved, What the Market Missed, and Why Governance Wins the Agentic Era

Palantir’s “NVIDIA moment” is here: Q1’s 85% growth and 145 Rule of 40 validate AIP’s compounding platform fit while governance moats secure the agentic era.

Summary

- Q1 validated the "NVIDIA moment" thesis: 85% YoY revenue growth, 54% FCF margins, and a Rule of 40 score of 145% confirm AIP's platform-market fit is triggering compounding demand acceleration.

- The market is concerned about agentic disruption risk: our Cursor parallel — where the fastest-scaling B2B SaaS company ever thrived despite direct competition from foundation model players — illustrates why Palantir's application-layer moat is far more durable than sentiment suggests.

- Model-layer dependency is the one risk worth watching: unlike Cursor, Palantir cannot freely adopt Chinese open-source models to differentiate, though its ontological data assets offer a clear path to proprietary model-layer differentiation over time.

- Jevons' Paradox and governance are complementary forces: collapsing inference costs will explosively expand the agentic TAM, but only platforms with deep orchestration and governance — Palantir's core strengths — can reliably serve it.

The Quarter That Validates the Thesis

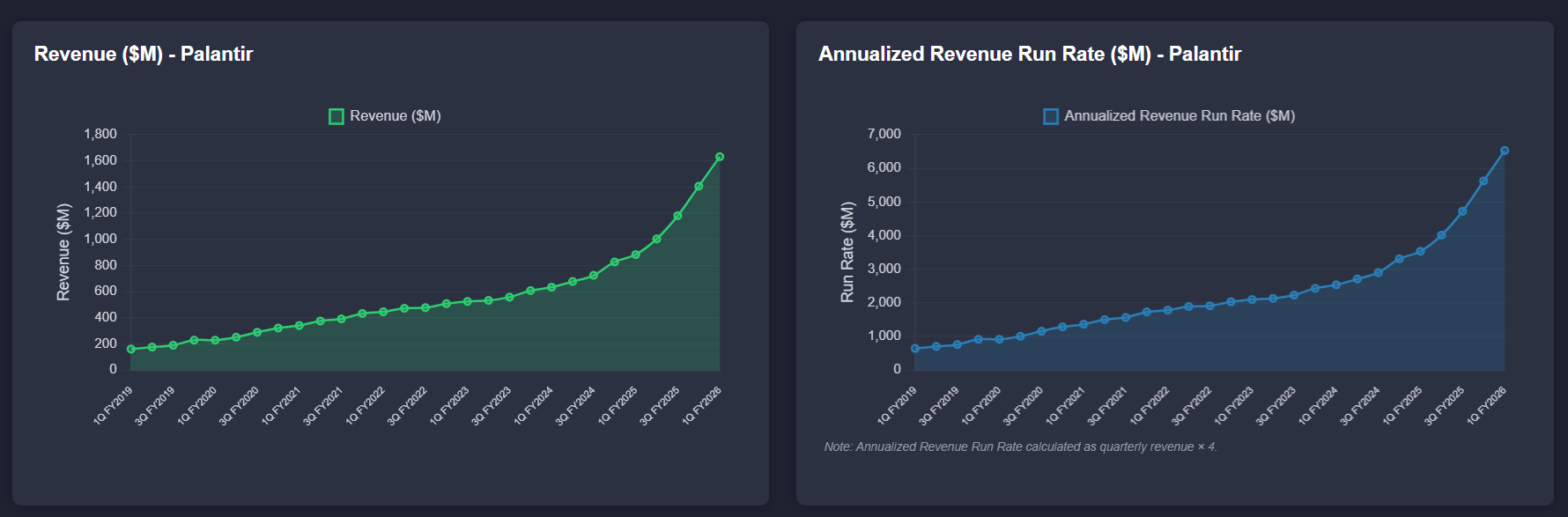

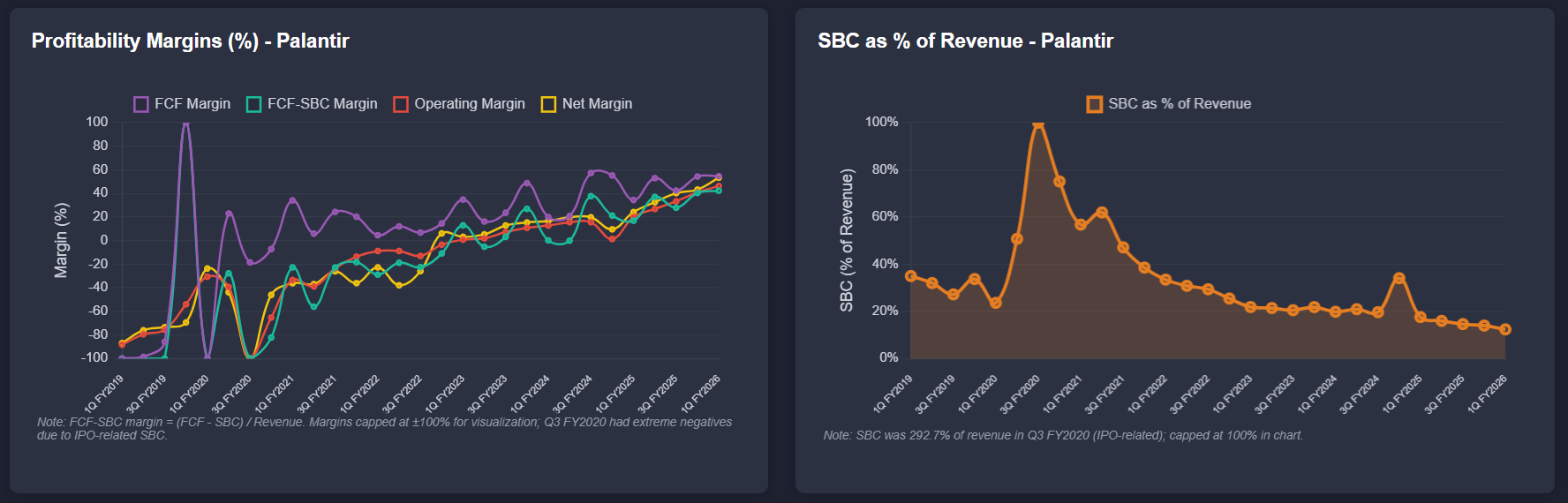

Palantir delivered a quarter that should confirm AIP is the best and only platform to securely plant AI models onto enterprises' environments. Revenue hit $1.633B, up 85% YoY and up 16% QoQ. U.S. revenue surged 104% to $1.282B, with U.S. Commercial exploding 133% to $595M and U.S. Government growing 84% to $687M. GAAP operating income reached $754M — a 46% margin. Our calculated FCF margin (cash from operations minus capex, divided by revenue) came in around 54%, with adjusted FCF margin at 57%. It's kind of crazy that PLTR's free cash flow in 1Q26 is greater than its total revenue in 1Q25. The Rule of 40 score: 145%. Management raised full-year 2026 revenue guidance to approximately $7.65–7.66B, implying roughly 71% annual growth, up meaningfully from the prior ~61% guide.

Source: Convequity/Claude Opus 4.6

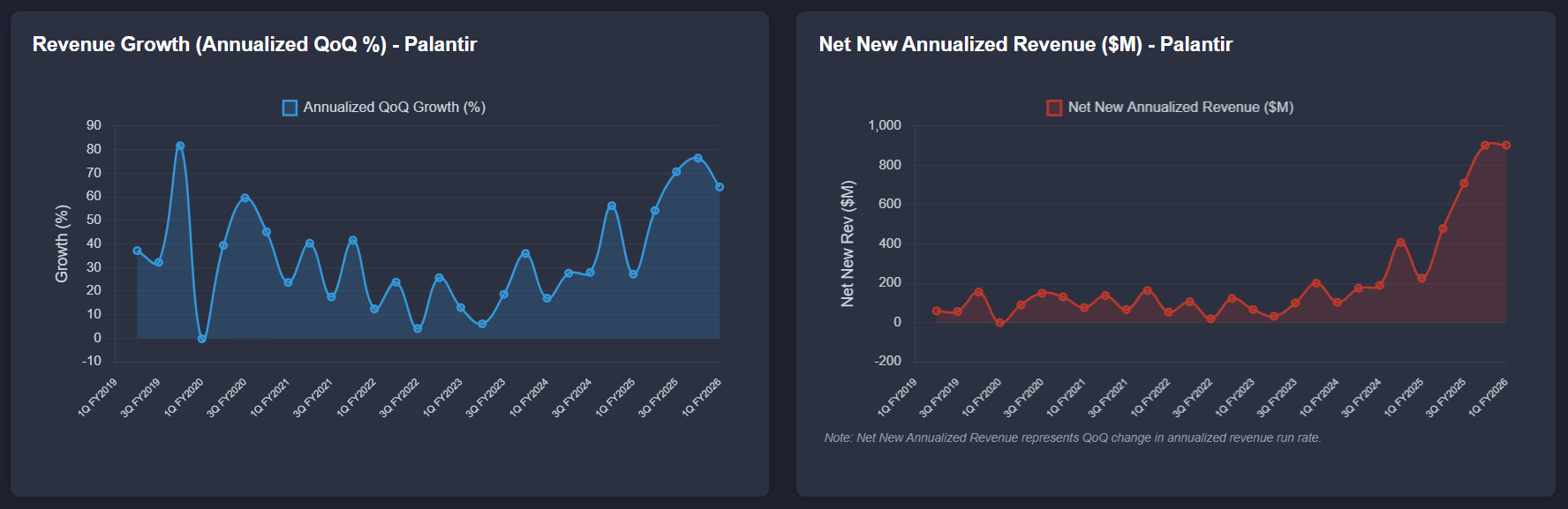

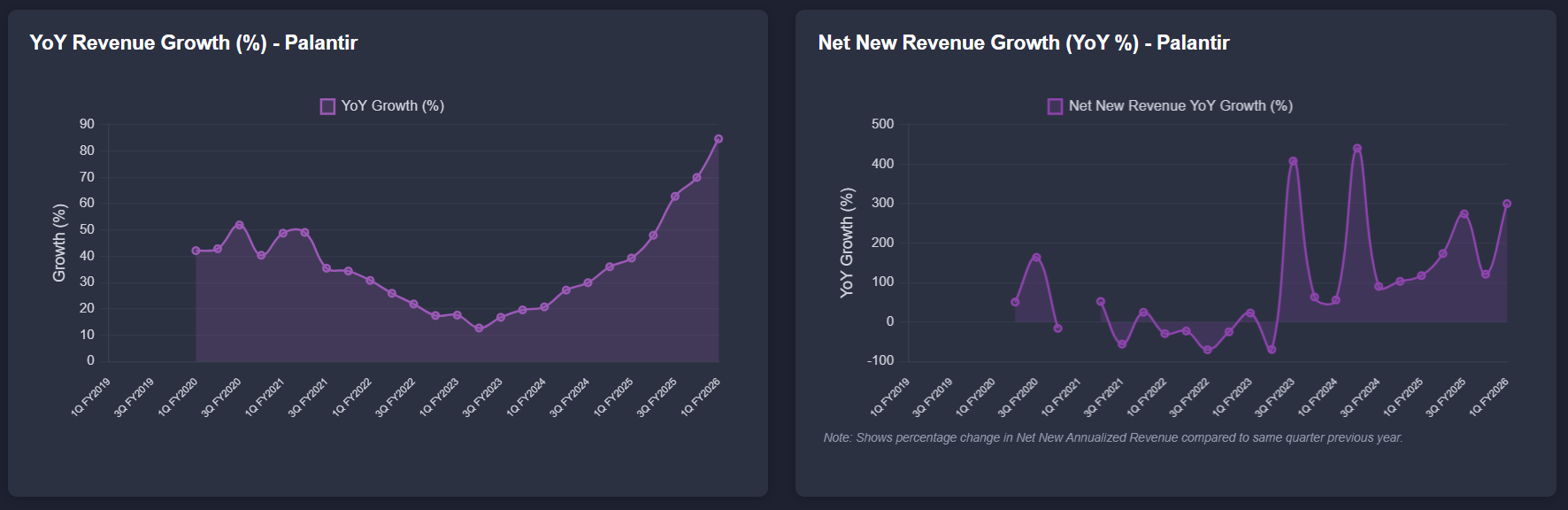

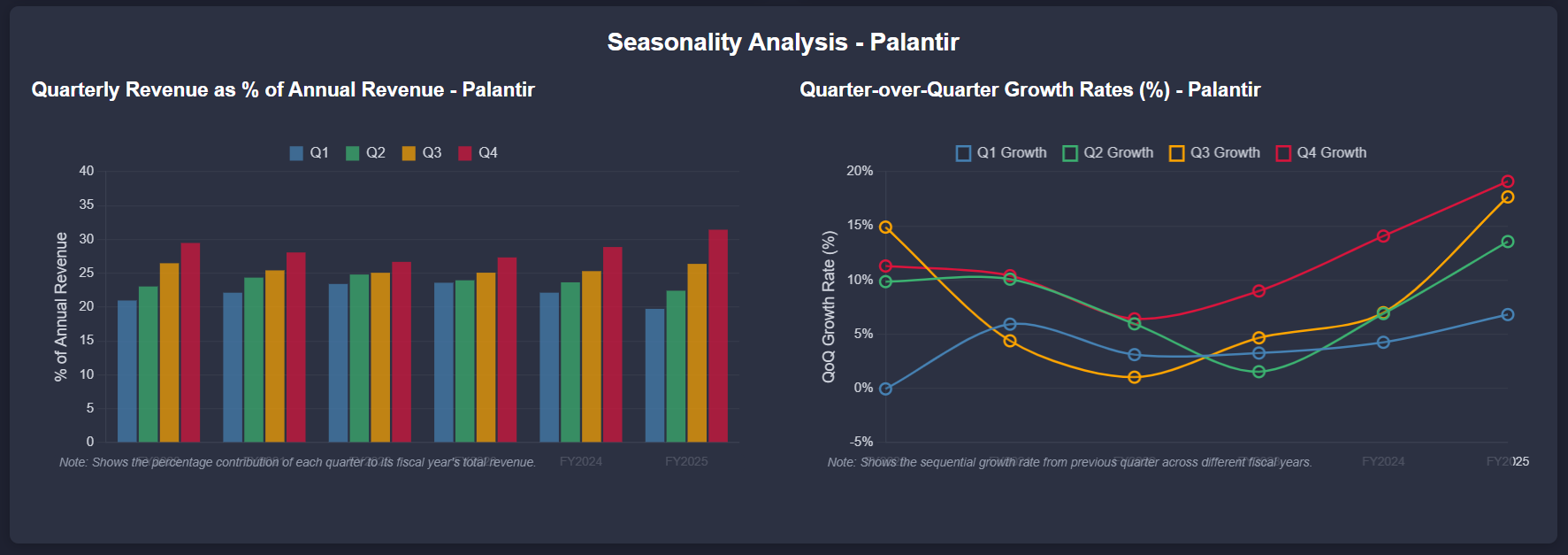

The charts above tell a clear story: revenue is compounding rapidly, margins have converged into best-in-class territory, SBC % has declined to ~14%, and net new revenue additions have exploded relative to the FY2022–FY2023 era. One metric investors likely honed in on is the annualized QoQ growth rate decelerating from approximately 76% in Q4 FY2025 to 64% in Q1 FY2026 — which at face value looks like momentum fading. But Palantir exhibits well-established seasonality: Q4 has historically been the strongest sequential quarter, benefiting from year-end budget flush and contract closures, while Q1 is typically the weakest. The seasonality chart confirms this unambiguously.

When PLTR was growing around 40% in early 2024, we told subscribers it was very possible the company would eventually experience its own "NVIDIA moment" — where platform-market fit triggers compounding demand that accelerates growth toward triple digits. That is now firmly materializing.

The thesis has always been about ontology. We've been saying this since early 2021. ChatGPT works for consumers because it was trained on the internet's curated ontologies. Enterprises lack that luxury — data silos and non-standard formats kill AI effectiveness. AIP married frontier AI models to bespoke customer ontologies, enabling real decisions and rapid iteration. The compounding has begun, and market penetration remains remarkably early at just over 1,000 customers.

ShipOS: Proof That the TAM Is Almost Incalculable

Perhaps the most consequential proof point this quarter is ShipOS, Palantir's platform for the U.S. Navy's shipbuilding industrial base. Bill-of-materials approvals were slashed from 200 hours to 15 seconds. Contract reviews accelerated 57–73%. Material planning time was cut by 94%. These are staggering efficiency gains inside one of the most complex, fragmented industries on earth.

China holds roughly 230x America's shipbuilding capacity. Modern conflict will hinge on drone swarms, AI strikes, hypersonics, and persistent global naval presence. Without a revitalized maritime industrial base, deterrence and power projection become much harder.

The strategic implications for investors are profound: if Palantir can transform shipbuilding — with its thousands of global suppliers, millions of parts, and decade-long programs — it proves these platforms can reshape virtually any critical industrial sector. That positions PLTR at the very center of America's reshoring push and reindustrialization agenda, functioning as the enabling layer for automation-first execution across major strategic industries. They will not create 10x capacity overnight, but by squeezing far more output from the existing base, ShipOS can eliminate bottlenecks, slash delays, and rebuild momentum that eventually compounds into real expansion.

The Agentic Disruption Concern

The annualized QoQ deceleration is not the only — or even the primary — reason for the muted post-earnings reaction. A deeper structural concern has weighed on sentiment: the fear that agentic AI from Anthropic, OpenAI, and others may disrupt the broader SaaS landscape — and that Palantir may not be immune.

Understanding this concern requires examining Palantir's evolving relationship with the foundation model layer. Initially, Palantir diversified its model layer strategically, integrating Mistral, LLaMA, and other open-source models alongside OpenAI and Anthropic to avoid over-reliance on any single closed-source provider. The logic was sound. But the competitive landscape has shifted: closed-source frontier models from OpenAI and Anthropic have pulled decisively ahead of open-source Western alternatives on capability benchmarks, particularly for the complex reasoning and multi-step agentic workflows that Palantir's enterprise customers demand. Despite still being model neutral, Palantir's commitment to delivering the best possible experience to its customers has thus increasingly locked the company into dependency on Western closed-source models — and this creates several interconnected risks.

First, reduced bargaining power and flexibility. As Palantir becomes more dependent on a small number of frontier model providers, those providers gain leverage — over pricing, over terms, and over the strategic relationship. This is the classic platform dependency risk, and it intensifies if Palantir's customers begin to associate the quality of Palantir's outputs with the quality of the underlying model.

Second, direct competitive entry. If OpenAI or Anthropic decide to enter Palantir's space — or even a few of its major verticals — they would be building on the same foundation models that power Palantir's platform, potentially achieving comparable product quality at the model layer while leveraging their own distribution and brand advantages. They would essentially have a similar quality product at the inference level, and would then be competing on the application and governance layers — where Palantir has deep advantages, but where the optics alone could suppress multiples. This is arguably the core scenario the market is digesting right now.

Third, geopolitical model constraints. Palantir is a prime contractor to the U.S. government and intelligence community. This almost certainly precludes the use of Chinese open-source models — DeepSeek, Kimi, and their successors — regardless of their technical merit. Palantir simply does not have the flexibility to adopt the best available models globally, irrespective of origin, to build differentiation versus the foundation model players' own vertical platforms.

This constraint has a compounding dimension. If Chinese open-source models continue to close the gap with — or surpass — Western closed-source models on key capability benchmarks, Palantir could find itself locked out of the highest-performing foundation models entirely. That would be detrimental from an entirely different angle than direct competitive entry — it would mean the best models in the world are the ones Palantir cannot use. The combination of all three risks — dependency on a small number of providers who may become competitors, using the same models as those potential competitors, and being unable to access potentially superior alternatives for geopolitical reasons — is a legitimate concern that warrants weight in any serious analysis.

The Cursor Parallel — And Why It Matters

The market's instinct to fear disruption from foundation model players is understandable — but recent history suggests it is often wrong, and the most instructive parallel is Cursor.