Notes: Convequity’s Lens on Software 3.0 Investing

Summary

- Software 3.0 mirrors the early internet era: AI is in an infrastructure-first phase where most value accrues to chips, data centers, power, and networking, while the true application winners largely do not yet exist.

- The public SaaS universe is structurally impaired, with slowing growth, high SBC, compressed multiples, and many companies “floating” below private-equity valuation floors without differentiated AI positioning.

- Legacy SaaS faces a scaling trap as per-seat models, curated human logic, and high-OPEX structures fail to translate into an AI era defined by outcomes, automation, and machine-driven workloads.

- AI reshapes both demand and supply: buyers become more rational through procurement AI, while builders ship cheaper and faster, squeezing high-margin, sales-led SaaS models from both sides.

- Near-term opportunity skews toward AI infrastructure, intermediate-term value emerges at the PaaS and tooling layer via talent diffusion from frontier labs, and long-term upside ultimately concentrates in AI-native software that has yet to be built.

Note: This analysis was written after reviewing 100+ public consumer tech, enterprise tech, semiconductor, and IT infrastructure companies.

Software 3.0, powered by deep learning, is disrupting the Software 1.0 and 2.0 paradigm. This mirrors the early 1990s, when foundational investment in hardware and semiconductors quietly set the stage for the next generation of software platforms that emerged in the 2000s.

Investing in software today feels as tedious as it did in the early 1990s because we are once again in an infrastructure-first phase of a platform transition. In that earlier period, the investable software universe was small not because opportunity was limited, but because the foundational layers — compute, networking, operating systems, and the public internet itself — were still being built. Most of the value at the time accrued to the underlying building blocks rather than to applications, and the true software explosion only followed once that infrastructure was in place in the late 1990s and early 2000s.

We see a strong parallel today. The investable AI-software universe is far smaller than the underlying building blocks that will ultimately support it — semiconductors, data centers, networking, and foundation models. As in the 1990s, maximum uncertainty surrounds the application layer: many of today’s software companies will not survive the transition, and many of the eventual AI giants have not yet been founded. But when the infrastructure matures, the payoff at the software layer is likely to be disproportionate, just as it was for the internet-native leaders that emerged two decades ago.

Crucially, this is not a “different” setup from the 1990s — it is the same dynamic repeating. Then, software- and internet-native companies disrupted hardware-centric and brick-and-mortar incumbents. Today, AI-native companies will increasingly disrupt SaaS-native incumbents. The disruptor eventually becomes the disrupted. The presence of an existing software ecosystem does not negate the parallel; in the 1990s, hardware, PCs, and enterprise IT already existed too. What changed was where intelligence, leverage, and economic power migrated.

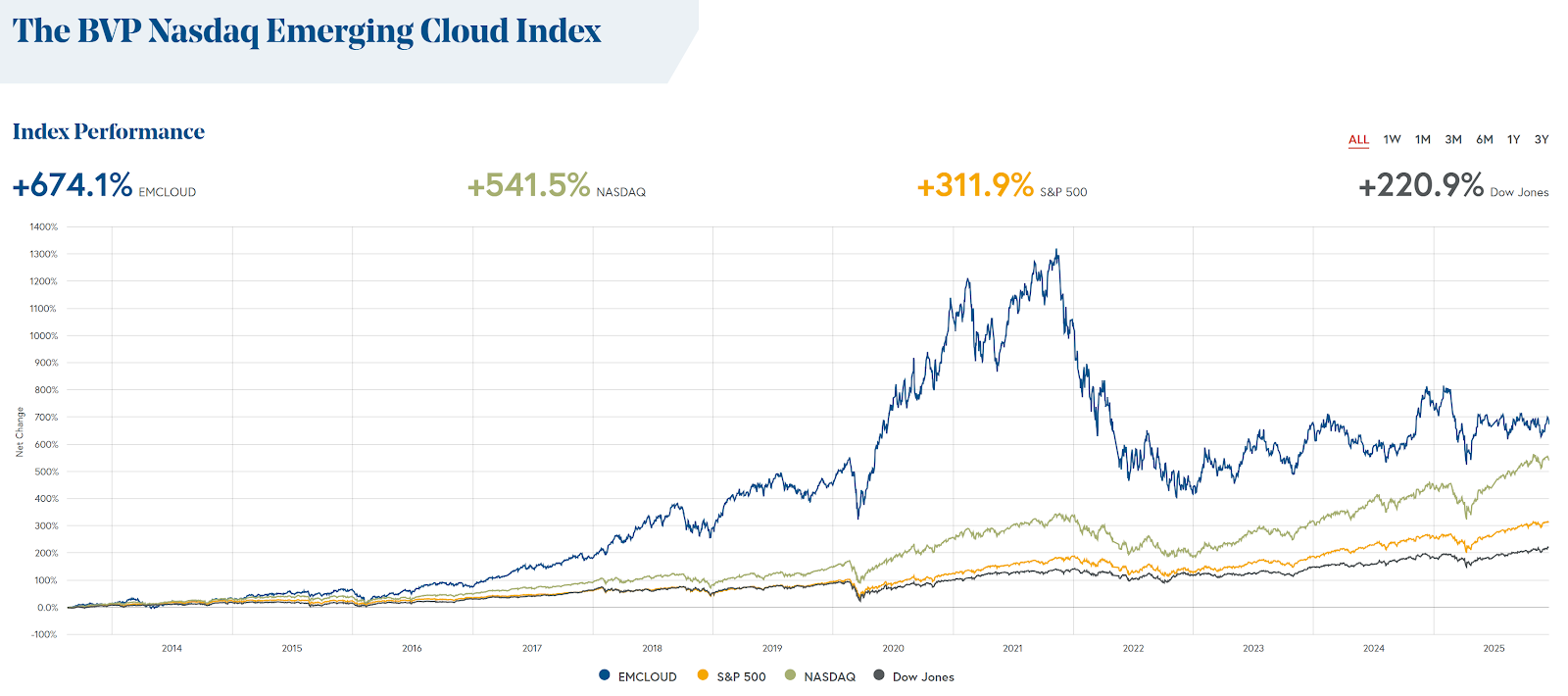

For investors, the implication is similar to that earlier era. In the early stages of a platform shift, most value accrues to infrastructure, while the application layer remains narrow, fragile, and difficult to underwrite. Only later — once the rails are fully laid — does a broad and durable software universe emerge. As a result, passively following today’s SaaS indices, such as Bessemer’s Emerging Cloud Index, risks anchoring portfolios to the outgoing paradigm, just as doing so in the mid-1990s would have missed the true internet-native winners that defined the following decade.

The all-time performance for this index looks impressive, outperforming the Nasdaq, S&P 500, and needless to say, the Dow Jones. However, as the chart reveals, the right side of the curve looks ugly. Zoom in, and that's where the cracks appear. Even over the past year, when tech has performed well and there have been pockets of hype across data and software, the index delivered negative returns and even underperformed the Dow Jones.

The explanation is straightforward: SaaS in general has experienced significant growth deceleration, while many young SaaS scale-ups continued executing growth-mode playbooks amid weakening top-line expansion. The entire software sector now shows growth in the mid-teens and margins in the high teens, resulting in 5–6x EV/S multiples.

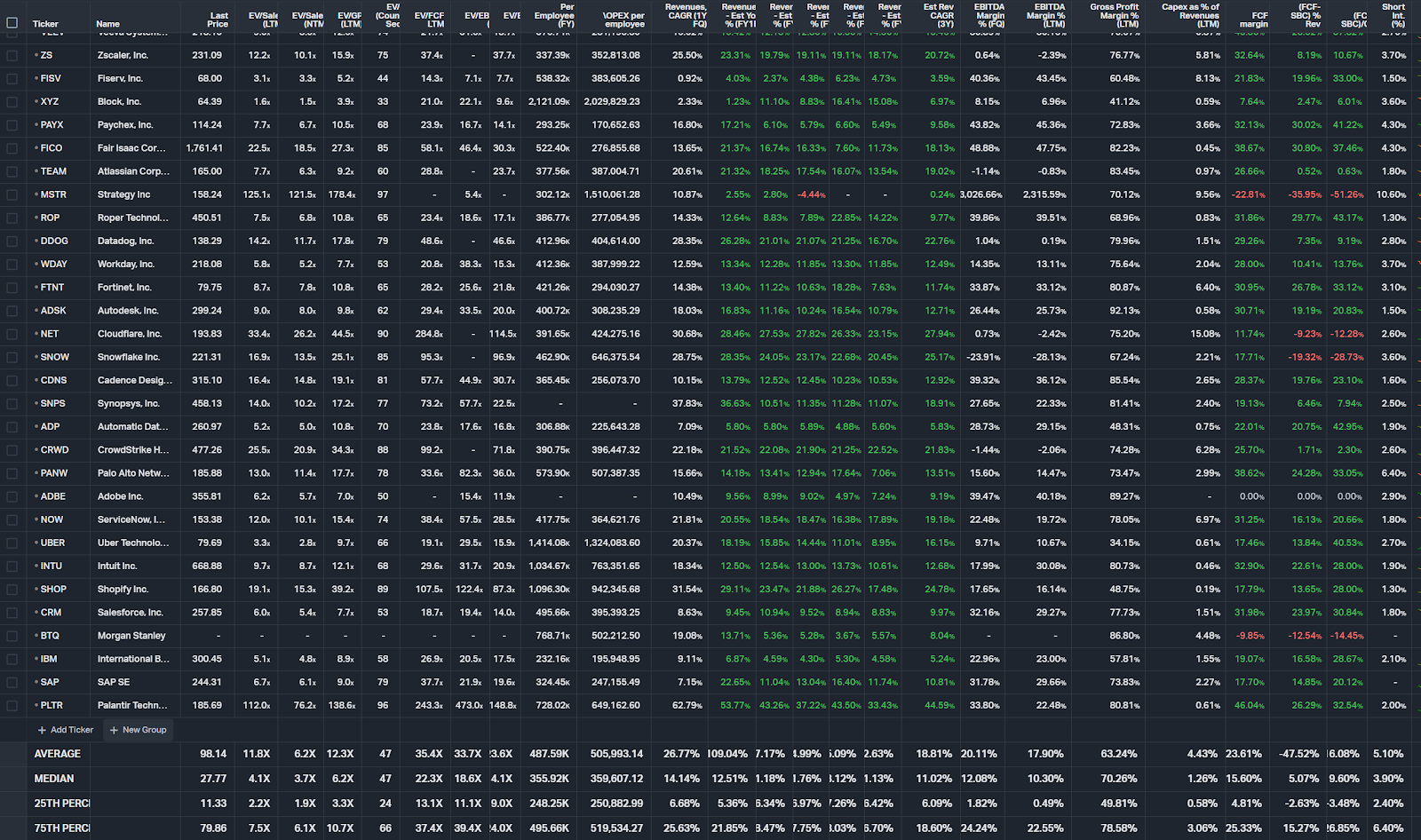

Source: Koyfin - Convequity All Software Watchlist

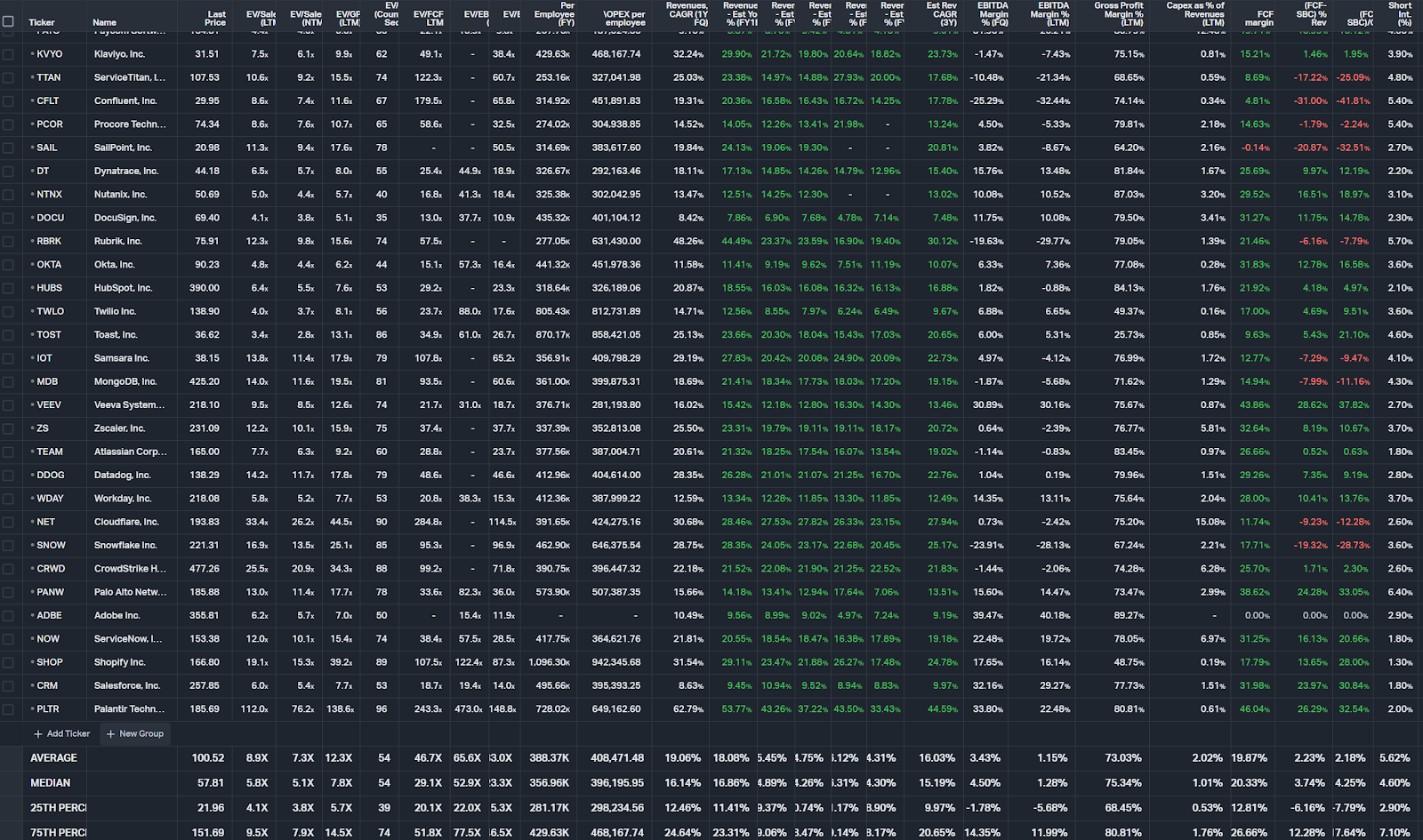

Source Koyfin - BVP EmergingCloud Index (ECI) Watchlist

EV/S Below PE Valuation Floors

We consider an EV/S of 5–6x to be "floating dead" because anywhere below that threshold, private equity can simply take the company private, eliminate unnecessary staff, boost margins to 30%+, and generate profits while maintaining low-teens growth. A restructured company of this kind should be worth at least 20x EV/EBIT, or approximately 6.7x EV/S assuming a 33% EBIT margin.

Across all software watchlists, the average, median, 25th percentile, and 75th percentile EV/S NTM figures are 6.2x, 3.7x, 1.9x, and 6.1x, respectively. For the ECI specifically, those numbers are 7.3x, 5.1x, 3.8x, and 7.9x.

The implications are stark: more than half of the software sector trades at roughly half of PE's floor valuation, and more than half of the formerly "emerging cloud" names now trade below that floor. In practical terms, a vast number of software companies are simply floating — doing nothing differentiated or valuable — much like a non-tech sector with no discernible future.

The median quarterly revenue growth for all software stands at just 14% with 70% gross margin, while FCF margin sits at 15.6% — dropping to just 5% after subtracting stock-based compensation. For the ECI, growth is slightly higher at 16% with 75% gross margin, and FCF margin reaches 20.7% — but falls to 3.7% after adjusting for SBC.

The picture is clear: the SaaS sector in general displays slightly higher growth, slightly better unit economics, and higher FCF margins on a headline basis. But due to elevated SBC, the adjusted FCF and GAAP margins are actually lower. This raises the critical question: are you willing to pay higher premiums for companies with marginally higher growth but substantially higher stock-based dilution? This dynamic may be the largest driver of the ECI's underperformance in recent years, as the sector broadly failed to embrace the operating efficiency discipline that Meta and Google adopted.

The Scaling Trap

We have observed numerous pre-2022 SaaS scale-ups — companies like Confluent and GitLab — caught in the middle phase of scaling when their growth engines suddenly began cracking. The software industry's general payback period runs around 30 months, a timeframe that seemed entirely reasonable in the pre-2022 era but now appears almost unimaginably long.