(Free) Fortinet: An Alternative Play On The SASE Narrative - ASIC Powers Multiple Catalysts, $200 Target Price

Read the report for free on Seeking Alpha.

Executive Summary

ASIC advancements, SD-WAN capabilities, impressive Fabric third-party ecosystem, and recent acquisitions to bolster automation, machine learning capabilities, and SASE, have all come together to form a very appealing approach to security that will support strong revenue growth in many years to come. Due to their core competency in appliance-based security and how they’ve adapted to deliver cloud-based security, Fortinet (FTNT), along with Palo Alto Networks (PANW), is one of the strongest vendors for hybrid use cases. And this on-premise/cloud dual capability ideally positions them to prosper in the cloud and edge computing evolutions.

Short-Term Outlook

Revenue

Had it not been for the COVID-19 headwinds FTNT would have seen accelerating sales in relation to their SD-WAN integrated security solutions. Considering the challenges, FTNT has delivered strong SD-WAN driven sales; 7 out 48 $1m+ deals in 3Q20 compared to 8 out of 53 $1m+ deals in 3Q19, and at the $250k+ deal threshold the number of SD-WAN deals have tripled YoY according to management in the 3Q20 earnings call. Taking into account FTNT’s inclusion as a ‘Leader’ of the highly reputed Gartner Magic Quadrant for WAN Edge Infrastructure in the final week of FTNT’s 3Q20, SD-WAN linked sales growth should accelerate going into 4Q20.

Moreover, an intra-vaccine environment further into CY21 should improve business conditions for SD-WAN deals and support top-line growth. We surmise that FTNT’s Americas sales have been hit by the U.S. being a cloud/SaaS adoption leader. Americas YoY revenue growth for 1Q20, 2Q20, and 3Q20 has been 20.9%, 15.6%, and 13.0% highlighting the difficult pandemic business conditions of late. In light of relatively fewer pure SaaS consumption options, U.S. customers focused on cloud-first transformations appear to have shunned FTNT for other younger cloud-native vendors.

Source: Gartner (August 2020)

FTNT does have high-quality cloud-delivered security alternatives though at present they are mainly bundled into appliance-based or VM license arrangements and less into pure SaaS consumption, or ‘pay-as-you-go’ models. Therefore, the main drawback from a customer perspective is likely the consumption model rather than the capabilities of FTNT’s cloud-based solutions. However, given that FTNT do actually offer some pure SaaS consumption-based solutions such as FortiCASB and FortiMail, it is likely that more will be added in quarters to come. Further SaaS consumption additions coupled with a greater push by S&M could comfortably get FTNT back on track in the cloud security market, in our opinion, therefore this is not too much of a concern to us.

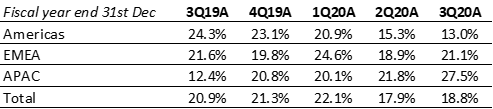

The WFH dynamic is another reason for the sharp deceleration in the Americas as the region has been hit harder with restrictions than other parts of the world. This has hampered FTNT’s on-prem sales growth as workforces have moved from office to home and other vendor cloud-based solutions have stepped in to fill in the security gaps. The following table presents YoY quarterly revenue growth rates by geography. EMEA had a blip in 2Q20 but showed some recovery in 3Q20 whilst APAC growth has accelerated. We surmise that the APAC growth ramp-up is attributed to FTNT’s investments in the region more than anything specifically COVID-19 related. The magnitude of the YoY growth response appears closely tied to the WFH mandates per region.

Source: FTNT website

In summary, FTNT’s growth slowdown in the Americas is mainly a result of the U.S. economy being hit harder with WFH mandates and, in the large part, U.S. based organizations wanting a cloud-first transformation having a preference for vendors with a greater range of pure SaaS consumption solutions compared to FTNT. In the next few quarters, we expect FTNT to reverse some of this deceleration by virtue of 1) the recent recognition as a Gartner Leader in the WAN Edge Infrastructure (aka SD-WAN) market, 2) improved on-prem business conditions in light of an intra-vaccine environment, and 3) more SaaS consumption models being rolled out for FTNT’s broad range of cloud-delivered security solutions.

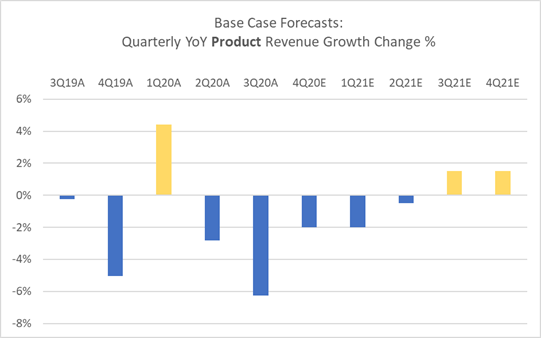

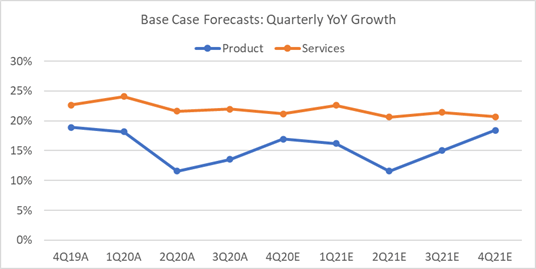

We anticipate points 1 and 2 will prevent further drops in YoY growth in product revenue in 4Q20E, 1Q21E, and 2Q21E and begin to lift growth in 3Q21E and 4Q21E as presented in the chart below.

Source: Convequity analysis

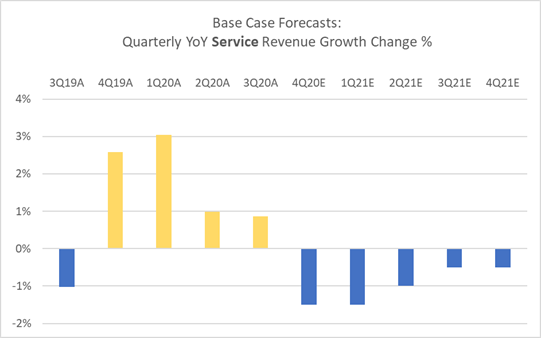

The next chart illustrates the change in YoY growth of service revenue from 3Q19A and our Base Case forecasts through 4Q21E. As a result of numerous subscription additions at the back-end of FY19 (CY19) FTNT’s YoY service revenue growth accelerated into 4Q19A and 1Q20A. Growth has still climbed fractionally higher during the pandemic, though as pointed out earlier, the remote working conditions has sparked a preference for security not only delivered from the cloud but also that can be consumed as a ‘pay-as-you-use’ basis – particularly in the U.S – which has had a countering effect on FTNT’s service revenue. Taking into account that service revenue, in absolute terms, is double that of product revenue, we expect market forces will decelerate service revenue growth regardless in quarters to come. However, we believe point 3, wherein FTNT adds in more ‘pay-as-you-go’ consumption options to their cloud solutions, will somewhat offset this and pull service growth to almost YoY flat in 3Q21E and 4Q21E.

Source: Convequity analysis

The following chart shows the historical and Convequity projections of YoY quarterly growth for both product and service revenue. In summary, by 4Q21E we project that points 1 and 2 will boost product growth and point 3 will offset a degree of the natural growth deceleration in service revenue.

Source: Convequity analysis

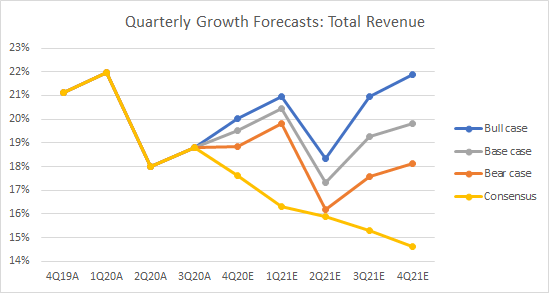

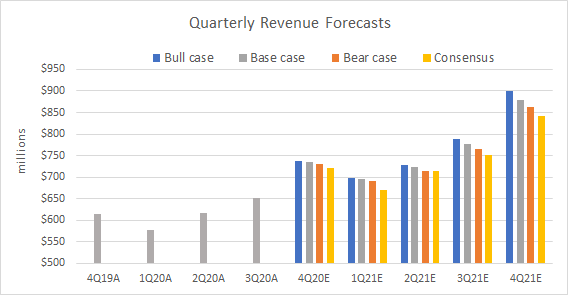

Our granular interpretation of recent growth and our forecasts at the category level translate into the following total revenue YoY growth projections and revenue amounts through 4Q21E.

Source: Convequity analysis

In our view the Bear Case materializes if intermittent economic lockdowns continue throughout CY21 despite the vaccine dissemination. This would result in large parts of the U.S. continuing to work remotely and hence negatively impacting FTNT’s on-prem business. The Bear Case is also likely to come to fruition if FTNT either fails to offer more SaaS/’pay-as-you-go’ consumption options or fails on the S&M side.

The Bull Case will likely transpire if the vaccine is widely disseminated, in the U.S. particular, by the 1st half of CY20 and some return to office life occurs, however, this is an unlikely scenario according to consensus expert opinion. Although, the Bull Case could still happen if FTNT makes progress with the consumption models for greater appeal to cloud-first customers while also generating greater appliance and VM sales to home bound employees. The latter sounds unlikely given the strength of the cloud trend though after taking into consideration the costs of FTNT’s all-in-one SD-WAN firewall/router designed for the home there are actually a few use cases whereby it is more cost effective than an alternative cloud solution. This customer-centric approach that lets the customer to decide whether appliance/VM or cloud is the better option for remote working could prove prosperous if FTNT pull the right levers.

We are truly surprised by the consensus expecting YoY growth will decline to 14.6% by 4Q21E. We feel that the plausible uplift in product revenue growth in an intra-vaccination world is underappreciated and in general the collective analyst view appears to overlook the aforementioned granular events likely to unfold in the next few quarters. Instead, they have merely extrapolated a downward growth trajectory irrespective of context.

$200 Target Price: SASE Not Currently Priced In

Much of FTNT's SD-WAN prowess and market opportunity appears to be priced in to date. SD-WAN driven growth was the key contributor to the 3-month rally from 2nd Oct-19 through 6th Feb-20 when the share price appreciated 60% to reach $121 and then climbed to $152 in Jul-20 during the stock market rebound from the Mar-20 crash. The latest catalyst, however, that doesn’t seem to be priced in is FTNT’s recent SASE progress.

Tech research giant Gartner, first coined the SASE term, or Secure Access Service Edge, in Aug-19 to describe the convergence of networking and security that will be increasingly needed as corporate networks are transformed from the ‘castle and moat’ model to highly distributed and remote infrastructures. Since then, networking and security vendors have made a beeline to offer this integrated service in attempt to be a leader in a promisingly high growth market. The cloud is a central component of Gartner’s SASE vision as it aligns with the trend of solutions being delivered as a service rather than from an on-premise box – opex over capex. Therefore, legacy vendors including FTNT, with high levels of technical debt, have found it harder than others to pivot to this SASE architecture. Since the introduction of SD-WAN in 2018, FTNT has been able to deliver integrated networking and security in one solution, though, this was done via an on-prem appliance. However, in Jul-20, FTNT purchased startup Opaq to acquired a critical SASE component – Zero Trust Network Access, or ZTNA. Prior to the acquisition, FTNT delivered ZTNA – which is a security concept that enables remote employees to securely access apps and greatly minimizes cyberattack opportunities – though it was conducted from within the on-prem appliance. Now they have Opaq on board, they can supply ZTNA from a location external to the corporate premises, or from the cloud, which provides far greater flexibility and simplicity for the customer, and thrusts FTNT into the SASE conversation.

The following chart of FTNT’s share price illustrates how FTNT’s SASE progress isn’t currently priced in. In Jun-20, Gartner released market guide for ZTNA and covered many vendors, both cloud-native and legacy, including Virginia-based Opaq but did not mention FTNT. Unsurprisingly, FTNT’s share price was a little choppy while cloud-native vendors trended upwards and even legacy rival Palo Alto Networks (PANW) climbed higher following the Gartner report. In quick response to the perceived gaps in the portfolio, FTNT purchased Gartner-recognized ZTNA leader Opaq in Jul-20. There was a brief pre-acquisition rally to a new high of $152, that we speculate could have been driven by insider knowledge of the impending deal but on the whole, there hasn’t been any meaningful market reaction. Since the Opaq acquisition the stock has struggled on the apparent lack of enthusiasm for FTNT’s crucial new addition to its SASE objectives. In the last week, however, upside momentum has broken the downward trend and closed the week ending 18th Dec-20 at $146 – only $6 under the all-time high.

Source: Convequity analysis

In our opinion, new highs will begin to price in the SASE progress and signal that the market finally appreciates FTNT’s strengthened competitive position. It feels like the next week might be a critical milestone for the stock and a rise above the all-time high of $152 reinforces our intrinsic DCF valuation of $200 that we forecast will be reached in c. 11 months. At $200, based on consensus NTM revenues of $2.86bn and 165.6 million shares, P/S NTM equates to 11.6x, which may seem high based on history though when compared to inferior SASE opponents like Zscaler (ZS) that are trading at 37x P/S NTM it seems plausible (even if the absolute revenue levels are not apples-to-apples).

Longer-Term Outlook

SaaS Conversion

We view FTNT to be in an ideal position to navigate the evolution and interactions of the cloud and edge industries – probably better placed than any other cybersecurity vendor. The Sunnyvale-based vendor isn’t considered a trailblazer within cloud trends though they have kept up with developments in the industry; they can provide a full stack of in-line inspection at PoPs and can deliver cloud-native security such as SecDevOps and CASB among other services. As mentioned earlier, the main drawback is FTNT’s pricing for cloud services – the majority of solutions are bundled into appliance or VM license agreements rather than allowed to be consumed in a ‘pay-as-you-go’ SaaS model. However, it is only a matter of time until FTNT can work through this and provide more customer-friendly pricing transparency. When this occurs, they will enhance their appeal to cloud customers. Furthermore, by having more solutions in pure SaaS consumption form will enable FTNT to reap the benefits of the greater transparency of the cloud marketplaces. Customers will be able to easily compare FTNT’s solutions against alternatives and we suspect their elite performance and market-leading Total Cost of Ownership, or TCO, will shine through.

The Edge

FTNT are undoubtedly a forerunner in the nascent computing edge, which some technology experts claim will become a larger industry than the cloud, and is expected to offer greater growth opportunities during the next few years (assuming the security segment grows at the same rates). Research firms estimate the edge will grow at a 20%-50% CAGR through 2025 compared to the cloud growing circa 19% CAGR. As FTNT has already built difficult-to-emulate competitive advantages in delivering security for edge devices we project that this industry will provide the greater future growth. FTNT’s distinct competitive advantages have been nurtured for two decades, right from the founding of the company back in 2000, and centres around the hardware integration – very rare for a predominantly enterprise software vendor. At its inception, founder and CEO Ken Xie, envisaged that eventually CPUs will not have the power to efficiently conduct all the functions required for effective cybersecurity. And lo and behold this has turned out to be correct as the constant deluge of traffic, the growing decryption/re-encryption demands, and the continual need for lower latency for real-time applications, has created huge bottlenecks that a standard computer chip, or CPU, can’t handle in a timely manner. Off the back of this epiphany Xie began developing the Application-Specific Integrated Chip that could focus on specific security tasks in order to increase the computing power of FTNT’s solutions. Due to the expensive nature of ASIC development and the extremely long lead times, no other cybersecurity firms followed suit – the risks of not knowing how the industry would evolve was too great to justify spending tens of millions of dollars on a project that might become obsolete in a couple of years. FTNT took the risk and it has paid off. Now, FTNT has the market-leading TCO and their hardware prowess has opened up the opportunity to enter the networking space which they have capitalized on with their Secure SD-WAN solutions.

The Importance of SD-WAN in SASE

The SD-WAN will become an increasingly critical component as the edge market develops. In 2019, Gartner introduced the term of SASE – the convergence of networking and security into one solution – and it’s becoming clear why this is crucial. As devices under the IoT umbrella proliferate and the world becomes hyperconnected in the era of 5G, a significant portion of security will need to be conducted where the user is located. For example, data packets flowing to and from self-driving vehicles cannot be sent to the cloud for inspection because it will add too much latency, therefore it needs to be done at the location of the machine and/or user. In essence, any application/device relying on critical real-time data will need security conducting at the location of the machine/user – in other words, the edge. Once security is completed at the edge, SD-WAN technology will be required to optimally route certain pieces of data to the nearest PoP for deeper analytics to support the real-time applications. Therefore, latency is still crucial for the edge to cloud (cloud to edge) journey. This is the space we envisage FTNT developing solid USPs and competitive advantages, because except for Palo Alto Networks (PANW), there is no other security or network vendor that can do both the security inspections and intelligently route traffic to maximize user experience - and this is all powered by FTNT’s ASIC superiority. And although PANW now have a SD-WAN integrated security solution, they have had to acquire startups to achieve this and therefore FTNT have a clear advantage in terms of intrinsic knowledge that has ramifications ranging from future innovations to customer deployments.

Cloud/Edge Summary

In summary, FTNT is a few years ahead of the competition in regards to all-in-one networking and security solutions, and this is attributed to their long history of ASIC-related investments and the incredible long-sighted vision of their founder and CEO. As a result, when the edge industry hits a meaningful market size (c. $16.5bn) in CY25 FTNT will have another growth driver. Ultimately, this is why we view FTNT as one of the best long-term investments in cybersecurity, and even more broadly, the enterprise software arena. While investors wait for the opportunities of the edge to really come to fruition, FTNT’s growth catalysts are SD-WAN integrated security, which is an essential infrastructure building block to enable a hyperconnected edge computing environment, and the various cloud security trends. FTNT doesn’t stand out from the crowd in regards to cloud security, though as previously mentioned they are competitive and will continue to win deals for hybrid use cases in particular. Therefore, the knowns are that the cloud and the edge are going to be huge growth opportunities for cybersecurity vendors in the future; a major unknown is whether the edge, or computing decentralization, will grow to be the more important paradigm, or will it continue to be the cloud, or the centralization theme. In either direction FTNT is set to prosper with long-term growth levers. Lastly, FTNT’s capabilities of delivering elite performance via appliance, VM, and in SaaS form factors facilitates a customer-centric strategy that exudes agility for forthcoming market dynamics in years to come.

FTNT Revenue Growth vs Industry

The following chart outlines FTNT’s revenue growth in comparison to the cybersecurity industry’s – historical and forecasts. Even by CY27, when we project annual Base Case sales will have surpassed $6bn, we project FTNT will be growing sales above the industry growth rate.

Source: various market research CAGR forecasts and Convequity analysis

In terms of market share, we estimate FTNT’s revenue growth trajectory will increase their share of the cybersecurity software industry – currently estimated at $73bn – from 3.2% in FY20E to 5.0% by FY27E. Considering the fragmentation of the industry and super growers such as Crowdstrike (CRWD), Zscaler (ZS), and Okta (OKTA), along with ultra-aggressive competitors such as PANW, such an increase in market share reflects our very positive view of FTNT’s long-term prospects.

Source: various market research CAGR forecasts, EDGAR, and Convequity analysis

In effect, out of the legacy vendors (all those excluding the super growers previously mentioned), we only envision FTNT and PANW gaining market share in years to come. If FTNT ever became more aggressive and/or effective in S&M and made a couple of higher risk acquisitions, their market share could conceivably be closer to 7% by CY27E. The reader may also notice that we anticipate the ‘Other’ vendor market share will decrease from 75% in CY20E to 63% in CY27E as a consequence of industry consolidation. In order to remain in the cybersecurity conversations, the legacy players will need to participate in M&A. However, drastic consolidation is unlikely given the plethora of business opportunities that will arise under the scope of IoT and the edge.

Long-Term Revenue Growth Forecasts

The long-term revenue growth scenario outcome is largely dependent on the evolutionary interaction between the edge and the cloud – with a growing dominance of the former being more beneficial to FTNT. It is also dependent on how FTNT can deliver all solutions as a service, or SaaS, and allow customers to consume all solutions on a ‘pay-as-you-go’ basis. We’re not concerned about FTNT’s ability to innovate, or be a fast follower, to engineer high-quality solutions because they have a long history of proving they are exceptional at this. Therefore, the main variables for FTNT’s future success are the central/decentralization narrative and the consumption models.

Source: Koyfin, Convequity valuation model

Other Growth Considerations

- In-house technological development: Due to FTNT’s engineering ego, it is rare that they indulge and spend their substantial cash balances on M&A subjects. They rather build a solution from the ground-up which is partly enabled by cheaper talent sourcing and the company’s culture also plays an instrumental part in this. One of the main rewards for this approach are the smoother deployments for enterprise customers because the solutions are easier to integrate as one compared to a multi-solution stitched together via M&A. Software management and troubleshooting are additional end-user benefits. This will continue to elevate FTNT’s brand and help minimize wasted investments in M&A to carry on channeling funds to value adding expenditures.

- Fabric is the Broadest Security Platform Around: Industry consolidation is currently being driven by two factors: 1) CISOs want simpler security management and to be away with the innumerable point solutions that there SOC teams have to manage; 2) Legacy security vendors need to remain relevant and the quickest way to gain new technologies is to purchase startups. FTNT have a huge advantage to capitalize on this consolidation trend by having the broadest security platform, Fabric. Moreover, they have the upper hand over other legacy vendors striving for platform success as a consequence of their ground-up ethos. In cases where a niche solution can’t be quickly developed in-house, the Fabric platform is loaded with high-quality APIs to integrate other vendors’ software.

- Strong International Government Business: FTNT have not yet cultivated a solid presence in the U.S. Federal market though they have compensated for this with strong revenues with international governments. And we see this as a better long-term growth driver than a stronger focus on the domestic Fed market – such as is the case with PANW – due to the diversification benefits. We also surmise that there are less painstaking regulatory pressures to meet when dealing with other governments leading to lesser drain on resources. Furthermore, governments managing in higher growth economies are less likely to push for discounts. On the whole, FTNT’s position within the international government market is very pro-long-term growth.

- SASE Infrastructure One of the Most Advanced After Opaq Acquisition: In July 2020, FTNT purchased Opaq for an undisclosed sum, though we estimate between $100m to $130m given the $43.5m in funding received since its launch in 2017. This has added cloud-based Zero Trust Network Access, or ZTNA, to FTNT’s portfolio and makes them a leader in the SASE space. Before the acquisition, FTNT delivered ZTNA via the appliance or VM, though now that Opaq is on board they can conduct ZTNA closer to the end user, or at the edge, and therefore reduce latency and improve user experience. The acquisition, in effect, does add the final piece to the SASE puzzle for FTNT – they now have the SD-WAN capability, the cloud-based in-line inspection processed at high speeds, the ZNTA, the MFA, the SWG, the CASB, the cloud workload protection, and through AI/ML integrated into their Fabric platform, are able to continually monitor and respond to risks.

- A Contrarian Approach to SASE May Further Increase Competitive Advantages: FTNT’s alternative approach appears to be the reason the financial markets are yet to price in the growth upside to their SASE repertoire. Since Gartner coined the term in 2019, vendors have hurried to put together a SASE architecture precisely how the research giant describes it – which entails the in-line security inspections occurring at PoPs, or the cloud, but as close to the user as feasible. Security functions being processed as close as possible to the user without being in-branch results in low latency and zero security devices for network administrators to manage. And this is why vendors have raced to build out far-reaching global PoP infrastructures to deliver these benefits and be regarded as a true SASE player. FTNT have followed suit but have also insisted that SASE can still be delivered in on-prem appliances and that the management of their all-in-one firewall is negligible compared to the previous headache of needing to maintain and upgrade multiple devices to ensure the necessary network and security. This is a fair point, given that traditionally to conduct effective network and security an organization needs a router, a firewall, a SWG, load balancer or optimizer, and a VPN device. FTNT’s long-held hardware focus has culminated in all these solutions being packed into one device, the FortiGate NGFW. And as the SD-WAN component makes the management of network devices infinitely easier, FTNT’s on-prem solution is still a big improvement. Therefore, we view FTNT’s all-in-one on-prem solution as a best of both worlds, or at least a middle ground, between the desire for security to be processed as close to the end user as possible for optimal latency, and the desire for zero device management. There will be many use cases for FTNT’s all-in-one on-prem solution, however, if an organization prefers the cloud-based approach FTNT can deliver that as well. As a result, FTNT have fostered a very customer-centric approach and have positioned themselves to be agile amid the unknowns of SASE/edge/cloud developments. Lastly, the underlying factor that empowers FTNT to create such a powerful all-in-one network and security device is their ASIC development which enables them to manufacture at very low costs.

Conclusion

FTNT's short-term drivers for revenue growth are the recent recognition as a Leader for WAN Edge Infrastructure by Gartner, a soon-to-be intra-vaccination environment that brings more of the office back into work life, and further 'pay-as-you-go' SaaS consumption options for cloud products. These drivers will maintain YoY growth close to 19%, in our opinion. In regard to the $200 target price, we view the c. $150 level as the threshold for SASE beginning to be priced in. A break higher would achieve all-time highs and be evidence that the market is finally taking note of the Opaq acquisition, making $200 doable in the foreseeable future.

In the longer-term FTNT has ideally positioned. Their Fabric platform is the broadest around and has a great opportunity to exploit the fragmented industry and appeal to CISOs' demand for vendor/solution consolidation. On the SASE front FTNT stand out on two levels. Firstly, they are the only vendor to have organically developed security and networking and seamlessly integrated the two. Secondly, they can deliver security-driven networking within the appliance/VM, or via the cloud - PANW is the only other SASE competitor able to do this but they haven't developed the networking element organically like FTNT have.

All-in-all the future looks very bright for FTNT. We believe it is the best all-round cybersecurity business there is and a great long-term investment.

Comments ()